Jan 30, 2025

This is the latest installment in our blog series, where we explore key reasons to send a press release—this time focusing on business...

Washington, D.C.--(Newsfile Corp. - December 30, 2019) - The Securities and Exchange Commission today announced that it is proposing amendments to codify certain staff consultations and modernize certain aspects of its auditor independence framework. The proposed amendments would update select aspects of the nearly two-decade-old auditor independence rule set to more effectively structure the independence rules and analysis so that relationships and services that would not pose threats to an auditor’s objectivity and impartiality do not trigger non-substantive rule breaches or potentially time consuming audit committee review of non-substantive matters.

“The proposed amendments are based on years of Commission staff experience in applying our auditor independence rule set and respond to recent and longer term feedback received from a wide range of market participants,” said Chairman Jay Clayton. “The proposal is consistent with the Commission’s long-recognized view that an audit by an objective, impartial, and skilled professional enhances both investor protection and market integrity, and, in turn, facilitates capital formation. In practice, the proposed amendments also would increase the number of qualified audit firms an issuer could choose from and permit audit committees and Commission staff to better focus on relationships that could impair an auditor’s objectivity and impartiality.”

Since the initial adoption of the auditor independence framework in 2000 and revisions in 2003, there have been significant changes in the capital markets and those who participate in them. The proposed amendments primarily focus on fact patterns presented to Commission staff through consultations that involve a relationship with, or services provided to, an entity that has little or no relationship with the entity under audit, and no relationship to the engagement team conducting the audit. In these scenarios (including the examples outlined below), the staff regularly observes that the audit firm is objective and impartial and, as a result, does not object to their continuing the audit relationship with the audit client.

The public comment period will remain open for 60 days following publication of the proposing release in the Federal Register.

* * *

Highlights

The Commission proposed amendments designed to modernize certain auditor independence requirements. Many of the current independence requirements have not been updated since their initial adoption in 2000 and amendments in 2003. Since that time, the Commission and our staff have, through several consultations per year, continued to learn about the application of our independence rule set and the efficiency and effectiveness of our independence requirements as market conditions and industry practices have changed. The proposed amendments to Rule 2-01 are designed to respond to these changes, reflect the SEC staff’s experience administering the independence requirements, and incorporate consideration of the recent and longer term feedback received from the public.

Aspects of Current Rules that Do Not Impact Audit Firm Objectivity and Impartiality

The following examples, based, in part, on the SEC staff’s consultation experience, help to illustrate some of the concerns with the current rules that the proposals would address.

Example 1 – Student Loans

Audit Firm has an audit partner based in Atlanta who continues to pay his student loans taken to attend college before starting his career at Audit Firm. A different audit partner in Atlanta audits the lender that provided the student loan, a large student loan company that originates thousands of student loans. Under the current rules, the student loan of the audit partner who is not part of the audit would still lead to an independence violation for the audit engagement of the lender.

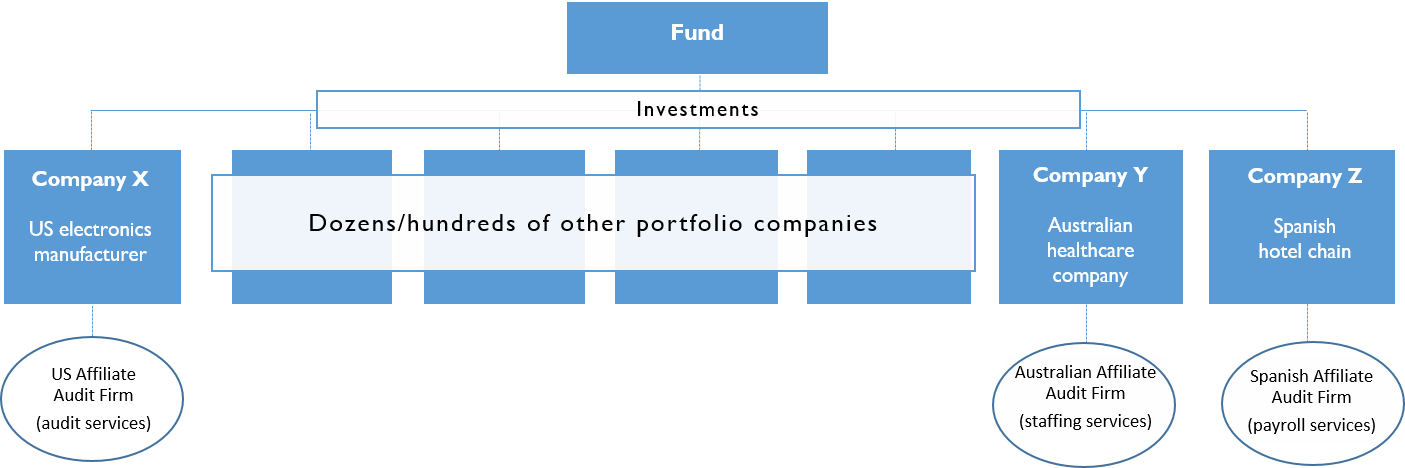

Example 2 – Portfolio Companies

Assume Company X is a U.S.-based portfolio company of Fund F. Fund F invests in various companies around the globe, perhaps dozens or even hundreds, including Company X. Audit Firm A is the auditor of Company X. Also assume that two of Audit Firm A’s global network affiliates provide the services discussed below to two separate portfolio companies of Fund F. Call them Company Y and Company Z. Further assume that Company Y and Company Z have no relation to each other or to Company X except for the fact that Fund F is invested in each Company. To add practical context, further assume that:

Also assume that Company X has its own separate governance structure that is unrelated to Company Y or Z, and Company Y and Z are not material to Fund F. Under the current auditor independence rules, if Company X registers with the SEC (e.g., by conducting an IPO), Audit Firm A would not be independent of Company X as a result of the services provided to either Company Y or Z. This is the case regardless of whether, as the SEC staff has observed in similar situations, these limited services at immaterial portfolio companies (Companies Y and Z) have no impact on the entity under audit in any way and do not impact the objectivity and impartiality of the auditor in conducting the audit for Company X.

The intent of the proposed amendments to the auditor independence rules is to avoid requiring Company X, under these and similar circumstances, to (1) replace Audit Firm A with another audit firm, (2) wait to register with the SEC for up to three years after termination of the services provided to Company Y and Company Z, or (3) make a determination, likely in consultation with Commission staff and/or the audit committee, that the rule violation did not impair the auditor’s objectivity and impartiality.

In some situations, the existing audit firm cannot be replaced as a practical matter because all other qualified audit firms have themselves provided services or established other relationships with portfolio companies of Fund F that triggered a breach of our independence rule. The issue of the independence rule set affecting auditor choice is brought home by this example and has increased significantly as the asset management industry has grown, investments have become more global and the global audit services ecosystem has consolidated and become more specialized.

The hypothetical scenario described above is based directly on SEC staff’s experience over the past decade. For the 12-month period ending September 30, 2019, the SEC staff has conducted a number of consultations in which this fact pattern, or one similar to it, was raised to the SEC staff by the registrant’s audit committee and its auditor, and the SEC staff, under such circumstances, did not object to the auditor’s and the audit committee’s conclusion that the auditor’s objectivity and impartiality would not be impaired. SEC staff has provided similar feedback in these types of scenarios over the past decade.

Proposed Amendments to Rule 2-01

The proposed amendments would, if adopted:

What’s Next?

The public comment period will remain open for 60 days following publication of the proposing release in the Federal Register.

###

Analyst, journalist, or company stakeholder? Sign up to receive news releases by email for Newsfile SEC Press Digest or all companies belonging to the Banking/Financial Services industry.