Cadia PC1-2 Feasibility Study demonstrates strong financial returns

Feasibility Study estimated IRR of 18% and NPV of US$1.4 billion over a 16 year mine life1,2,3,4

Confirms Cadia's position as a world class, long-life gold and copper producer

Optimised mine footprint with additional ore mined across the life of the project

Increased annual gold and copper production compared to the Pre-Feasibility Study

Early works continue to progress well, with first gold and copper production anticipated in FY265

Melbourne, Australia--(Newsfile Corp. - November 10, 2022) - Newcrest Mining Limited (ASX: NCM) (TSX: NCM) (PNGX: NCM) is pleased to announce that the Newcrest Board has approved progression of the Cadia PC1-2 Feasibility Study (the Study) to the Execution Stage.

The Study represents the next panel cave for execution at Cadia after PC2-3 and forms a key strategic milestone for Newcrest to maintain Cadia's long-life production profile, with the development of PC1-2 accounting for approximately 20% of Cadia's published Ore Reserves. The Study contemplates a high lift, undercut block cave producing up to 25 million tonnes1,2 of crushed ore per annum at a very attractive rate of return. First production from PC1-2 is expected in FY26, with execution targeted for FY295.

The Early Works Program remains on track with key development activities and raise boring currently underway. Preliminary earthworks to support construction of the primary ventilation system are also in progress.

Newcrest Managing Director and Chief Executive Officer, Sandeep Biswas, said, "We are very pleased to announce the findings of the Cadia PC1-2 Feasibility Study today, which indicates strong financial returns and underscores the quality of this world class asset. Together with the Cadia Expansion Project which is nearing completion, we are confident that Cadia will continue to be an outstanding gold and copper producer for decades to come."

"Through applying our technical expertise in deep underground mining and value breakthrough strategies, our team has further optimised the PC1-2 mine footprint since the Pre-Feasibility Study, creating a more efficient cave and substantially increasing expected ore production across the life of the project. We now expect to deliver additional gold and copper production over the next decade and beyond, which is an outstanding achievement by our team and a great example of our innovation and creativity in action."

"We also have significant financial headroom to fund the construction of PC1-2 through our internal cash flow and prudent use of our strong balance sheet. This further underpins Cadia's ability to continue contributing to the community and we remain focused on pursuing further optimisations during the Execution Stage of the project," said Mr Biswas.

Summary of Study Findings1,2,3,4

Substantial gold and copper production growth compared to the Pre-Feasibility Study (PFS) in a Tier 1 jurisdiction

~16 year mine life from first production, at an average of 17Mt per annum

Total ore production of 280Mt producing 3.7Moz of gold and 670kt of copper

Average annual gold production of 231koz and copper production of 42kt from PC1-2

Attractive investment returns

Estimated total capital expenditure on a real basis of ~A$1.4 billion (~US$1.1 billion) and a nominal basis of ~A$1.6 billion (~US$1.2 billion)

Real, after-tax Internal Rate of Return (IRR) of 18%

Net Present Value (NPV) of A$1.8 billion (US$1.4 billion)

Average All-In Sustaining Cost (AISC) of A$198/oz (US$148/oz) on a real basis

Enhanced footprint design and productivity compared to the PFS, including:

Adapting the well proven extraction level layout used at Cadia East to increase ore mined and significantly improve safety

Increasing gold and copper production with additional ore mined over the mine life

Optimising the materials handling system with two crushing stations north and south of the footprint to improve efficiency, utilisation and reduce production loss

- Early works program funding of A$120 million (~US$90 million) approved in August 2021, with preliminary works on ventilation systems and other critical path development activities already in execution

Table of Key Study Findings1,2,3,4

| Area | Measure | Unit | PC1-2 Study Outcomes |

| Production | Average ore milled / throughput6 | mtpa | 17 |

| LOM | years | 16 | |

| Ore mined | mt | 280 | |

| Average gold grade | g/t | 0.49 | |

| Gold produced | moz | 3.7 | |

| Average annual gold production | koz | 231 | |

| Average copper grade | % | 0.27 | |

| Copper produced | kt | 670 | |

| Average annual copper production | kt | 42 | |

| Average gold recoveries | % | 83.2 | |

| Average copper recoveries | % | 88.0 | |

| Capital | Project capital (main works) | A$m (real) | 1,437 |

| Sustaining capital | A$m (real) | 1,195 | |

| Total life of mine capital | A$m (real) | 2,632 | |

| Operating | AISC | A$/oz sold (real) | 198 |

| Economic assumptions | Gold price | US$/oz (real) | 1,500 |

| Copper price | US$/lb (real) | 3.50 | |

| AUD:USD exchange rate | 0.75 |

Key Milestones5,7

Development of PC1-2 is expected to sustain total Cadia mine production at approximately 35 million tonnes per annum as production from the current operational PC1 and PC2 caves begin to decline from FY246. The first draw bell for PC2-3 was successfully fired in September 2022, with first production expected during the March 2023 quarter. The PC1-2 cave is expected to take approximately 6-7 years to reach its maximum production capacity following blasting of the first draw bell.

An indicative summary of key expected milestones is outlined below:

| Key project milestone | Date |

| First Production of gold / copper | FY26 |

| Execution Stage complete | FY29 |

Cadia's indicative production profile

Indicative gold and copper production profile1,6,7,8

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/7614/143874_0a11a544e45b4987_003full.jpg

Mine development and sequence1,6,7,8

| Panel Cave | Start Construction | First Production | Ore (Mt) |

| PC2-3 | In progress | FY23 | ~130 |

| PC1-2 | FY23 | FY26 | ~280 |

| PC1-3 | FY31 | FY32 | ~110 |

| PC3-1 | FY34 | FY37 | ~160 |

| PC2-4 | FY37 | FY39 | ~110 |

| PC1-4 | FY43 | FY45 | ~140 |

| PC5001 | FY45 | FY47 | ~75 |

| PC2-5 | FY51 | FY51 | ~20 |

Indicative ore production profile1,6,7,8

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/7614/143874_0a11a544e45b4987_004full.jpg

Indicative mine production profile1,6,7,8

| Period | Total Material Movement (Mt) | Plant Feed (Mt) | Average Gold Grade (g/t) | Average Copper Grade (%) |

| FY23 - FY25 | ~105 | ~105 | 0.5 | 0.3 |

| FY26 - FY28 | ~105 | ~105 | 0.4 | 0.3 |

| FY29 - FY31 | ~105 | ~105 | 0.5 | 0.3 |

| FY32 - FY34 | ~104 | ~104 | 0.4 | 0.3 |

| FY35 - FY37 | ~105 | ~105 | 0.5 | 0.2 |

| FY38 - FY40 | ~104 | ~104 | 0.5 | 0.3 |

| FY41 - FY43 | ~105 | ~105 | 0.4 | 0.3 |

| FY44 - FY46 | ~105 | ~105 | 0.4 | 0.3 |

| FY47 - FY49 | ~105 | ~105 | 0.4 | 0.3 |

| FY50 - FY52 | ~105 | ~105 | 0.4 | 0.2 |

| FY53 - FY55 | ~100 | ~100 | 0.4 | 0.2 |

| FY56+ | Remaining Ore Reserves if any, subject to ongoing study | |||

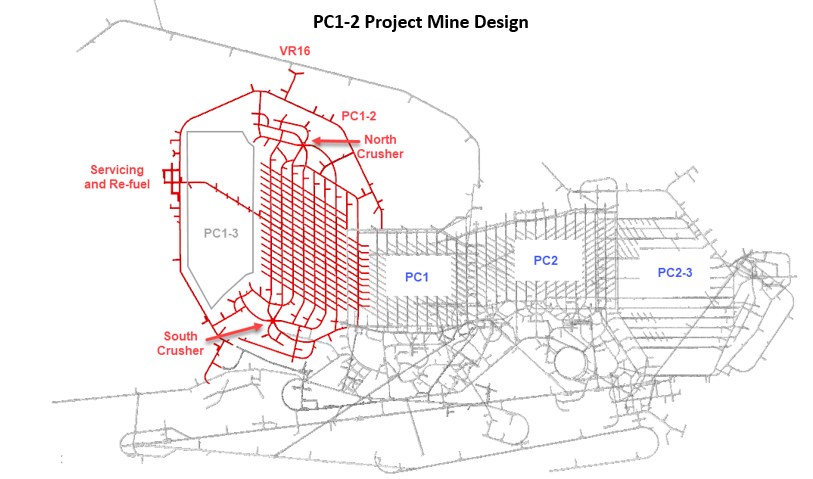

PC1-2 extraction level design

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/7614/143874_0a11a544e45b4987_005full.jpg

Metal price and exchange rate sensitivity analysis1,2,3,4

The actual IRR of the Study will vary according to the gold and copper prices realised. Base case assumptions include a gold price of US$1,500 per ounce, copper price of US$3.50 per pound, and an AUD:USD exchange rate of 0.75.

The table below outlines how the estimated Study IRR of 18% varies using different price assumptions:

| Scenario | Assumption (US$) | IRR (%) |

| Gold price (per ounce) | 1,250 | 15 |

| Gold price (per ounce) | 1,950 | 23 |

| Copper price (per lb) | 3.00 | 16 |

| Copper price (per lb) | 4.10 | 20 |

Estimated project capital expenditure profile1,3,4

Total capital expenditure for the main works phase development of PC1-2 is estimated to be approximately

A$1.4 billion (~US$1.1 billion) on a real basis, and approximately A$1.6 billion (~US$1.2 billion) on a nominal basis over the following years:

| Project capital expenditure (main works) | FY23 | FY24 | FY25 | FY26 | FY27+ | Total |

| Real | ||||||

| Project Capital Expenditure (A$m) | 139 | 297 | 329 | 260 | 411 | 1,437 |

| Project Capital Expenditure (US$m) | 105 | 223 | 247 | 195 | 309 | 1,077 |

| Nominal | ||||||

| Project Capital Expenditure (A$m) | 144 | 315 | 358 | 290 | 474 | 1,581 |

| Project Capital Expenditure (US$m) | 108 | 236 | 268 | 217 | 355 | 1,185 |

Cost assumptions and further optimisation opportunities

Changes in cost assumptions compared to the PFS are outlined below:

Project main works capital expenditure of A$1,437 million (real) is higher than the PFS project main works capital of A$1,122 million. The 28% cost increase is driven by a 10% increase in the extraction footprint, inflationary pressures, primarily across labour, contractors, steel, electricity and explosives, and an additional contingency allowance to account for increased volatility.

Sustaining capital expenditure of A$1,195 million (real) is ~2% higher due to inflationary pressures and additional costs associated with tailings storage, partly offset by value engineering.

Average All-In Sustaining Cost (AISC) across the life of the project of A$198/oz (US$148/oz) on a real basis is higher than the PFS AISC of A$54/oz (US$41/oz), mainly driven by higher operating costs, with inflationary pressures across labour, steel, electricity and processing consumables. In addition, copper recovery assumptions are lower, treatment and refining charges are increasing with market conditions deteriorating for shipping, freight, refining and smelting charges, and general and administrative costs are higher due to increasing insurance charges. These costs were partly offset by a higher copper price assumption.

Activities continue to be pursued to optimise the Study outcomes and reduce costs to maximise long-term value.

Newcrest continued to progress the early works program since the PFS release in August 2021, with A$74 million of capital expenditure incurred on key development activities, raise boring and earthworks to support construction of the primary ventilation system.

Permitting

Cadia presently holds a major Project Approval for the Cadia East Project until calendar year 2031 (inclusive of the permit to develop PC1-2).

In December 2021, Cadia received approval from the New South Wales Department of Planning, Industry & Environment for a modification to increase its permitted processing capacity from 32Mtpa to 35Mtpa6. The modification also provided approval for Newcrest to repair the slumped section of the Northern Tailings Storage Facility and revise the footprint of the NTSF and Southern Tailings Storage Facility to allow for a change from upstream to a centreline lift design.

Cadia has commenced planning for the long-term continuation of mining operations known as the Cadia Continued Operations Project (CCOP). Key aspects of the CCOP include a proposed development for a new Tailings Storage Facility adjacent to the current Southern Tailings Storage Facility.

Forward Looking Statements

This document includes forward looking statements and forward looking information within the meaning of securities laws of applicable jurisdictions. Forward looking statements can generally be identified by the use of words such as "may", "will", "expect", "intend", "plan", "estimate", "target", "anticipate", "believe", "continue", "objectives", "outlook" and "guidance", or other similar words and may include, without limitation, statements regarding estimated reserves and resources, internal rates of return, expansion, exploration and development activities and the specifications, targets, results, analyses, interpretations, benefits, costs and timing of them; certain plans, strategies, aspirations and objectives of management, anticipated production, sustainability initiatives, dates for projects, reports, studies or construction, expected costs, cash flow or production outputs and anticipated productive lives of projects and mines. The Company continues to distinguish between outlook and guidance. Guidance statements relate to the current financial year. Outlook statements relate to years subsequent to the current financial year.

These forward looking statements involve known and unknown risks, uncertainties and other factors that may cause the Company's actual results, performance, and achievements to differ materially from any future results, performance or achievements, or industry results, expressed or implied by these forward looking statements. Relevant factors may include, but are not limited to, changes in commodity prices, foreign exchange fluctuations and general economic conditions, increased costs and demand for production inputs, the speculative nature of exploration and project development, including the risks of obtaining necessary licences and permits and diminishing quantities or grades of resources or reserves, political and social risks, changes to the regulatory framework within which the Company operates or may in the future operate, environmental conditions including extreme weather conditions, recruitment and retention of personnel, industrial relations issues and litigation. For further information as to the risks which may impact on the Company's results and performance, please see the risk factors discussed in the Operating and Financial Review included in the Appendix 4E and Financial Report for the year ended 30 June 2022 and the Annual Information Form dated 6 December 2021 which are available to view at www.asx.com.au under the code "NCM" and on Newcrest's SEDAR profile.

Forward looking statements are based on management's current expectations and reflect Newcrest's good faith assumptions, judgements, estimates and other information available as at the date of this report and/or the date of Newcrest's planning or scenario analysis processes as to the financial, market, regulatory and other relevant environments that will exist and affect Newcrest's business and operations in the future. Newcrest does not give any assurance that the assumptions will prove to be correct. There may be other factors that could cause actual results or events not to be as anticipated, and many events are beyond the reasonable control of Newcrest. Readers are cautioned not to place undue reliance on forward looking statements, particularly in the current economic climate with the significant volatility, uncertainty and disruption caused by global events such as geopolitical tensions, the inflationary environment and rising interest rates and the ongoing COVID19 pandemic. Forward looking statements in this document speak only at the date of issue. Except as required by applicable laws or regulations, Newcrest does not undertake any obligation to publicly update or revise any of the forward looking statements or to advise of any change in assumptions on which any such statement is based.

Non-IFRS Information

Newcrest's results are reported under International Financial Reporting Standards (IFRS). This document includes certain non-IFRS financial information within the meaning of ASIC Regulatory Guide 230: 'Disclosing non-IFRS financial information' published by ASIC and 'non-GAAP information' within the meaning of National Instrument 52-112 - Non-GAAP and Other Financial Measures published by the Canadian Securities Administrator.

Such information includes All-In Sustaining Cost (AISC) and All-In Cost (AIC) as per updated World Gold Council Guidance Note on Non-GAAP Metrics released in November 2018. AISC will vary from period to period as a result of various factors including production performance, timing of sales and the level of sustaining capital and the relative contribution of each asset. AISC Margin reflects the average realised gold price less AISC per ounce sold.

These measures are used internally by Management to assess the performance of the business and make decisions on the allocation of resources and are included in this document to provide greater understanding of the underlying financial performance of Newcrest's operations. The non-IFRS information has not been subject to audit or review by Newcrest's external auditor and should be used in addition to IFRS information. Such non-IFRS financial information/non-GAAP financial measures do not have a standardised meaning prescribed by IFRS and may be calculated differently by other companies. Although Newcrest believes these non-IFRS/non-GAAP financial measures provide useful information to investors in measuring the financial performance and condition of its business, investors are cautioned not to place undue reliance on any non-IFRS financial information/non-GAAP financial measures included in this document. When reviewing business performance, this non-IFRS information should be used in addition to, and not as a replacement of, measures prepared in accordance with IFRS, available on Newcrest's website and the ASX and SEDAR platforms.

Ore Reserves, Mineral Reserves and Mineral Resources Reporting Requirements

As an Australian Company with securities listed on the Australian Securities Exchange (ASX), Newcrest is subject to Australian disclosure requirements and standards, including the requirements of the Corporations Act 2001 and the ASX. Investors should note that it is a requirement of the ASX Listing Rules that the reporting of Ore Reserves and Mineral Resources in Australia is in accordance with the 2012 Edition of the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves (the JORC Code) and that Newcrest's Ore Reserve and Mineral Resource estimates and reporting comply with the JORC Code.

Newcrest is also subject to certain Canadian disclosure requirements and standards, as a result of its secondary listing on the Toronto Stock Exchange (TSX), including the requirements of National Instrument 43-101 - Standards of Disclosure for Mineral Projects (NI 43-101). Investors should note that it is a requirement of Canadian securities law that the reporting of Mineral Reserves and Mineral Resources in Canada and the disclosure of scientific and technical information concerning a mineral project on a property material to Newcrest comply with NI 43-101.

Newcrest's material properties are currently Cadia, Lihir, Red Chris and Wafi-Golpu. Copies of the NI 43-101 Reports for Cadia, Lihir and Wafi-Golpu, which were released on 14 October 2020, and Red Chris, which was released on 30 November 2021, are available at www.newcrest.com and on Newcrest's SEDAR profile.

Competent Persons' Statement

The information in this document that relates to Ore Reserves has been extracted from the release titled "Annual Mineral Resources and Ore Reserves Statement - as at 30 June 2022" dated 19 August 2022 which is available to view at www.asx.com.au under the code "NCM" (the original release). Newcrest confirms that it is not aware of any new information or data that materially affects the information included in the original release and that all material assumptions and technical parameters underpinning the estimates in the original release continue to apply and have not materially changed, but are subject to depletions since 30 June 2022. Newcrest confirms that the form and context in which the Competent Person's findings are presented have not been materially modified from the original release.

Technical and Scientific Information

The technical and scientific information contained in this document was reviewed and approved by Philip Stephenson, Newcrest's Chief Operating Officer (Australasia), FAusIMM and a Qualified Person as defined in NI 43-101.

Authorised by the Newcrest Disclosure Committee

For further information please contact

Investor Enquires

Tom Dixon

+61 3 9522 5570

+61 450 541 389

Tom.Dixon@newcrest.com.au

Rebecca Lay

+61 3 9522 5298

+61 438 355 511

Rebecca.Lay@newcrest.com.au

North American Investor Enquiries

Vlada Cvijetinovic

+1 604 566 8781

+1 604 240 2998

Vlada.Cvijetinovic@newcrest.com.au

Media Enquiries

Tim Salathiel

+61 3 9522 4263

+61 407 885 272

Tim.Salathiel@newcrest.com.au

This information is available on our website at www.newcrest.com

Endnotes

1 The Feasibility Study has been prepared with the objective that its findings are subject to an accuracy range of ±10-15%. The findings in the Study and the implementation of the PC1-2 Project are subject to all the necessary approvals, permits, internal and regulatory requirements and further works. The Study estimates are indicative only and are subject to market and operating conditions. They should not be construed as guidance.

2 The production targets underpinning the Feasibility Study are contained in the column titled "PC1-2 Study Outcomes" in the table on page 2 under the heading "Table of Key Study Findings". The production targets are based on the utilisation of ~20% of the total Cadia East Ore Reserves as set out in the release titled "Annual Mineral Resources and Ore Reserves Statement - as at 30 June 2022" dated 19 August 2022 which has been prepared by Competent Persons in accordance with Appendix 5A of the ASX Listing Rules and is available to view at www.asx.com.au under the code "NCM" and on Newcrest's SEDAR profile.

3 As Cadia's functional currency is AUD, the Study has been assessed in AUD. The outcomes in this release have been converted to USD using an exchange rate of 0.75.

4 Using a discount factor of 4.5% (real).

5 Subject to market and operating conditions and no unforeseen delays.

6 The modification approved in December 2021 to increase the permitted processing capacity from 32Mtpa to 35Mtpa is subject to conditions including Newcrest commissioning an independent audit report to the satisfaction of the New South Wales Department of Planning & Environment Secretary in relation to Newcrest's approach to managing and minimising the off-site air quality impacts of the project.

7 The production targets are based on the utilisation of 100% of the total Cadia East Ore Reserves as set out in the release titled "Annual Mineral Resources and Ore Reserves Statement - as at 30 June 2022" dated 19 August 2022 which has been prepared by Competent Persons in accordance with Appendix 5A of the ASX Listing Rules and is available to view at www.asx.com.au under the code "NCM" and on Newcrest's SEDAR profile.

8 As described in the section titled "Permitting and Tailings", further approvals will be required for the throughput rate on which this is based and operations after 2031.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/143874

Source: Newcrest Mining Limited