{kind=link}

Sep 30, 2025

Legal and compliance press releases may not grab headlines like product launches or marketing campaigns — but they are among the most...

Ivanhoe Mines reports record profit of $351.5 million for Q2 2022

Kamoa-Kakula Mining Complex in the Democratic Republic of Congo sold record 85,794 tonnes of payable copper and recognized revenue of $494.1 million in Q2 2022

Kamoa Copper's cost of sales total $1.15 per pound of payable copper during the second quarter, with C1 cash costs of $1.42 per pound

Over the first half of 2022, Kamoa-Kakula milled approximately three million tonnes at 5.59% copper, and produced

142,916 tonnes of copper

Kamoa-Kakula produced record 32,877 tonnes of copper in July for an annualized production rate of 387,100 tonnes of copper

Platreef underground mining advancing well, with more than 200 metres of lateral development completed during the quarter

Johannesburg, South Africa--(Newsfile Corp. - August 15, 2022) - Ivanhoe Mines (TSX: IVN) (OTCQX: IVPAF) President Marna Cloete and Chief Financial Officer David van Heerden are pleased to announce the financial results for the three and six months ended June 30, 2022. Ivanhoe Mines is a leading Canadian mining company developing and expanding its four principal mining and exploration projects in Southern Africa: the Kamoa-Kakula Mining Complex in the Democratic Republic of Congo (DRC), which commenced commercial production in July 2021; the Platreef palladium, rhodium, nickel, platinum, copper and gold discovery in South Africa; the historic Kipushi zinc-copper-lead-germanium mine in the DRC; and the expansive exploration program for new copper discoveries on Ivanhoe's Western Foreland exploration licences, near Kamoa-Kakula. All figures are in U.S. dollars unless otherwise stated.

HIGHLIGHTS

Watch a July fly-over of mining and construction activities at Kamoa-Kakula: https://vimeo.com/739389126/d7bf137f91

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_002full.jpg

Kamoa Copper undertaking optimization of logistics costs

Due to the early commissioning and highly successful ramp-up of the Phase 2 concentrator during Q2 2022, Kamoa Copper dispatched approximately 177,000 tonnes of copper concentrates, a significant increase on approximately 103,000 tonnes dispatched during Q1 2022.

Copper C1 cash costs per pound of payable copper for Q2 2022 were higher than Q1 2022 largely due to a 42% increase in logistics charges for the transportation of Kamoa-Kakula's copper products.

The increase in logistics charges for the quarter were impacted by limitations in truck availability caused by the sharp increase in volumes, interrupted port operations at Durban caused by flooding, customs clearing times and border congestion between the DRC and Zambia, as well as higher diesel prices.

However, mine site operating costs are somewhat shielded from higher diesel prices, as site power is provided by the DRC national grid at a rate of approximately 6 cents per kilowatt hour, following the refurbishment of the Mwadingusha hydropower facility under a public-private partnership with Société Nationale d'Électricité (SNEL), the DRC state power utility company.

In addition, the Lualaba Copper Smelter located near Kolwezi, which is expected to treat approximately 150,000 tonnes of copper concentrates from Kamoa-Kakula annually, is undergoing scheduled maintenance that is expected to be completed in early September. Until then, Kamoa Copper's concentrate production will be wholly transported and exported as copper concentrate (approximately 50% contained copper), without the expected quantity of blister copper (approximately 99% contained copper), thereby temporarily increasing logistics costs.

Kamoa Copper, working alongside its offtake partners, Zijin Mining and CITIC Metal as well as the government of the DRC, is undertaking several initiatives to optimize the transportation of Kamoa Copper's products.

These activities include working with its offtake partners, logistics service providers and local entrepreneurs to increase regional trucking capacity, improving processes for clearing products for export and opening up alternative export borders between the DRC and Zambia. A second import-export border crossing recently was opened at Sakania, in addition to the existing border at Kasumbalesa, DRC.

Kamoa Copper is also working to increase flexibility to ship from a variety of ports, including Durban in South Africa, Dar es Salaam in Tanzania, Walvis Bay in Namibia and Beira in Mozambique, and longer-term to the port of Lobito in Angola.

A step-change improvement in cash costs of 10% to 20% is anticipated once Kamoa Copper's on-site 500,000-tonne-per-annum, direct-to-blister flash smelter is commissioned as part of the Phase 3 expansion, expected by the end of 2024. This cash cost reduction is in large part due to the significant decrease in volumes shipped, with approximately 600,000 tonnes of blister copper product shipped (including local toll smelting) instead of approximately 1.3 million tonnes of copper concentrate. In addition, the smelter will generate valuable by-product credits from the sale of sulphuric acid, which is in deficit in the DRC Copperbelt.

Kakula Mine optimization work targeting grades towards 6% copper

Ongoing mining optimization work at the Kakula Mine is targeting improved head grade during the second half of 2022 towards 6% copper. Kamoa Copper is also evaluating additional material handling capacity at Kakula to increase mining rates to feed the de-bottlenecked Phase 1 and 2 processing capacity of 9.2 million tonnes of ore per annum, which will be incorporated into the Phase 3 expansion Pre-Feasibility Study scheduled for the end of the year.

While the near-term expansion of underground infrastructure at Kakula takes place, ore will be drawn periodically from the surface stockpiles to maximize copper production as the Phase 1 and 2 concentrators are currently operating in excess of design capacity. As at the end of June 2022, Kamoa-Kakula's high- and medium-grade ore surface stockpiles totalled approximately 4.6 million tonnes at an estimated grade of 4.42% copper.

Management anticipates that the early commissioning of the Phase 2 concentrator plant in March 2022, approximately four months ahead of schedule, has enabled Kamoa Copper to increase the lower end of its full year 2022 production guidance from a range of between 290,000 to 340,000 tonnes of copper in concentrate, to between 310,000 and 340,000 tonnes.

Ivanhoe Mines' President Marna Cloete commented: "Ivanhoe Mines is very well positioned to manage the current commodity-market volatility and industry-wide inflationary pressures, with a strong balance sheet, tier-one, low-cost mining assets, and an experienced management team. Kamoa-Kakula is the fastest-growing, highest-grade major copper complex on the planet, and will be a long-life, cornerstone supplier of critical, high-quality, low-carbon copper metal. We remain extremely confident in copper's mid-to-long term fundamentals as the world navigates the transition to clean energy. The increase in Kamoa Copper's annual production guidance estimate is a further testament to the excellent work by the mine operations team during the Phase 1 and Phase 2 construction and ramp-up.

We are working closely with our partners to identify opportunities to improve the efficiency of Kamoa-Kakula's concentrate transport and logistics to mitigate any further cost pressures over the coming quarters. We are confident we can work proactively alongside the government of Democratic Republic of Congo to identify potential infrastructure pathways that improve our trucking and shipping conditions. With respect to Kamoa-Kakula's on-site costs, these have been largely insulated from the recent inflationary market conditions."

Ivanhoe Mines to host conference call for investors on August 15

The company will hold an investor conference call to discuss the Q2 2022 financial results at 10:30 a.m. Eastern time / 7:30 a.m. Pacific time on August 15. The conference call dial-in is +1-647-484-0258 or toll free 1-800-289-0720, quote "Ivanhoe Mines Q2 2022 Financial Results" if requested. Media are invited to attend on a listen-only basis.

Link to join the live audio webcast: https://bit.ly/3I7kaCR

An audio webcast recording of the conference call, together with supporting presentation slides, will be available on Ivanhoe Mines' website at www.ivanhoemines.com.

After issuance, the Financial Statements and Management's Discussion and Analysis will be available at www.ivanhoemines.com and at www.sedar.com.

Principal projects and review of activities

1. Kamoa-Kakula Mining Complex

39.6%-owned by Ivanhoe Mines

Democratic Republic of Congo

The Kamoa-Kakula Mining Complex, operated as the Kamoa Copper joint venture between Ivanhoe Mines and Zijin Mining, has been independently ranked as the world's fourth-largest copper deposit by international mining consultant Wood Mackenzie. The project is approximately 25 kilometres west of the town of Kolwezi and about 270 kilometres west of Lubumbashi. Kamoa-Kakula began producing copper in May 2021 and achieved commercial production on July 1, 2021.

Ivanhoe sold a 49.5% share interest in Kamoa Holding Limited (Kamoa Holding) to Zijin Mining and a 1% share interest in Kamoa Holding to privately owned Crystal River in December 2015. Kamoa Holding holds an 80% interest in the project. Since the conclusion of the Zijin transaction, each shareholder has been required to fund expenditures at Kamoa-Kakula in an amount equivalent to its proportionate shareholding interest. Ivanhoe and Zijin Mining each hold an indirect 39.6% interest in Kamoa-Kakula, Crystal River holds an indirect 0.8% interest, and the DRC government holds a direct 20% interest.

Construction of an additional scavenger-cleaner flotation cell at the Phase 1 concentrator, part of the de-bottlenecking program to boost copper production to approximately 450,000 tonnes per annum by Q2 2023.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_003full.jpg

Health and safety at Kamoa-Kakula

At the end of June 2022, Kamoa-Kakula reached 4,272,520 work hours free of a lost-time injury. Two lost-time injuries occurred underground at the Kakula Mine in Q2 2022. Kamoa Copper continues to strive toward its workplace objective of zero harm to all employees and contractors.

Nursing staff inside the new medical facility at the Kamoa Hospital.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_004full.jpg

Kamoa-Kakula summary of operating and financial data

| Q2 2022 | Q1 2022 | Q4 2021 | Q3 2021 | ||

| Ore tonnes milled | (000's tonnes) | 1,950 | 1,083 | 1,059 | 861 |

| Copper ore grade processed | (%) | 5.44% | 5.91% | 5.96% | 5.89% |

| Copper recovery | (%) | 84.0% | 87.1% | 86.4% | 83.4% |

| Copper in concentrate produced | (tonnes) | 87,314 | 55,602 | 54,481 | 41,545 |

| Payable copper sold | (tonnes) | 85,794 | 51,919 | 53,165 | 41,490 |

| Cost of sales per pound | ($ per pound) | 1.15 | 1.08 | 1.12 | 1.08 |

| Cash cost (C1) | ($ per pound) | 1.42 | 1.21 | 1.28 | 1.37 |

| Sales revenue before remeasurement | ($'000) | 699,381 | 467,453 | 458,880 | 355,022 |

| Remeasurement of contract receivables | ($'000) | (205,248) | 52,142 | 29,656 | (12,438) |

| Sales revenue after remeasurement | ($'000) | 494,133 | 519,595 | 488,536 | 342,584 |

| EBITDA | ($'000) | 286,313 | 399,391 | 357,619 | 233,212 |

| EBITDA margin | (%) | 58% | 77% | 73% | 68% |

C1 cash costs are prepared on a basis consistent with the industry standard definitions by Wood Mackenzie cost guidelines, but are not measures recognized under IFRS. In calculating the C1 cash cost, the costs are measured on the same basis as the Company's share of profit from the Kamoa Holding joint venture that is contained in the financial statements. C1 cash costs are used by management to evaluate operating performance and includes all direct mining, processing, and general and administrative costs. Smelter charges and freight deductions on sales to final port of destination, which are recognized as a component of sales revenues, are added to C1 cash cost to arrive at an approximate cost of delivered, finished metal. C1 cash costs exclude royalties and production taxes and non-routine charges as they are not direct production costs.

C1 cash cost per pound of payable copper produced can be further broken down as follows:

| Q2 2022 | Q1 2022 | Q4 2021 | Q3 2021 | ||

| Mining | ($ per lb.) | 0.39 | 0.30 | 0.27 | 0.36 |

| Processing | ($ per lb.) | 0.14 | 0.15 | 0.17 | 0.16 |

| Logistics charges (delivered to China) | ($ per lb.) | 0.51 | 0.36 | 0.37 | 0.35 |

| Treatment, refining and smelter charges | ($ per lb.) | 0.21 | 0.20 | 0.24 | 0.21 |

| General and administrative expenditure | ($ per lb.) | 0.17 | 0.20 | 0.23 | 0.29 |

| C1 cash cost per pound of payable copper produced | ($ per lb.) | 1.42 | 1.21 | 1.28 | 1.37 |

All figures in the above tables are on a 100%-project basis. Metal reported in concentrate is prior to refining losses or deductions associated with smelter terms. This release includes EBITDA, "EBITDA margin" and "Cash costs (C1) per pound" which are non-GAAP financial performance measures. For a detailed description of each of the non-GAAP financial performance measures used herein, and a detailed reconciliation to the most directly comparable measure under IFRS, please refer to the Non-GAAP Financial Performance Measures section of the Q2 2022 MD&A.

Record quarterly production of 87,314 tonnes of copper in Q2 2022

In late March 2022, Ivanhoe Mines announced that Kamoa-Kakula's Phase 2 concentrator plant began hot commissioning significantly ahead of schedule. First ore was introduced into the Phase 2 milling circuit on March 21, 2022, and first copper concentrate was produced approximately four months ahead of the originally announced development schedule. Commercial production from the Phase 2 concentrator was declared on April 7, 2022, while steady state production was achieved at the end of May 2022. During June 2022, copper recoveries were averaging more than 86%, with feed grades averaging approximately 5.5% copper.

Kamoa-Kakula set a new quarterly production record in the second quarter of 2022 with 87,314 tonnes of copper in concentrate produced, up from 55,602 tonnes of copper in concentrate produced in Q1 2022 and 54,481 tonnes of copper in concentrate produced in the fourth quarter of 2021. A total of 1.95 million ore tonnes were milled during the second quarter of 2022 at an average feed grade of 5.44% copper.

Over the first half of 2022, Kamoa-Kakula milled approximately three million tonnes of ore at an average feed grade of 5.59% copper, and produced 142,916 tonnes of copper in concentrate.

Phase 1 and Phase 2 debottlenecking project to boost throughput to 9.2 million tonnes of ore per year remains on schedule

Kamoa Copper's previously announced de-bottlenecking program is also progressing on schedule to increase the combined design processing capacity of the Phase 1 and Phase 2 concentrator plants to approximately 9.2 million tonnes per annum (from 7.6 million tonnes per annum).

After successfully commissioning and operating the Phase 1 and 2 concentrators, the Kamoa-Kakula team identified several relatively minor modifications that are expected to increase ore throughput from the current design of 475 tonnes per hour to approximately 580 tonnes per hour. These modifications include increasing the diameter of several pipes, replacing several motors and pumps with larger ones and installing additional flotation, concentrate-thickening, concentrate-filtration and tailings-disposal capacity. Detailed planning is underway to maximize the use of planned maintenance shutdowns of the concentrators for the installation of the new debottlenecking equipment, which is expected to take place later this year.

Once completed in the second quarter of 2023, the de-bottlenecking program will enable the copper production from Kamoa-Kakula's first two phases to reach approximately 450,000 tonnes per annum, positioning Kamoa Copper as the world's fourth largest copper producer.

Construction is advancing well on the additional tailings thickener at Kamoa-Kakula's Phase 1 and Phase 2 concentrator plants as part of the de-bottlenecking program.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_005full.jpg

Civil works are also advancing well for the planned installation of a fourth Larox filter press at Kamoa-Kakula's concentrate warehouse.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_006full.jpg

Safety Officer Franck Katende inspects construction of additional scavenger cleaner flotation capacity at the Phase 1 and Phase 2 concentrator plants.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_007full.jpg

Phase 3 Pre-Feasibility Study nearing completion

The Pre-Feasibility Study for the Phase 3 expansion is expected to be announced towards the end of this year. Kamoa-Kakula's Phase 3 will consist of two new underground mines, known as Kamoa 1 and Kamoa 2. A new, 5-million-tonne-per-annum concentrator plant will also be established adjacent to the two new mines at Kamoa. In addition, Kamoa-Kakula's Phase 3 expansion includes a 500,000-tonne-per-annum, direct-to-blister flash smelter to produce approximately 99% copper metal, and the replacement of Turbine #5 at the Inga II hydroelectric power station. The turbine replacement will supply an additional 178-megawatts (MW) of clean hydroelectric power to the national grid.

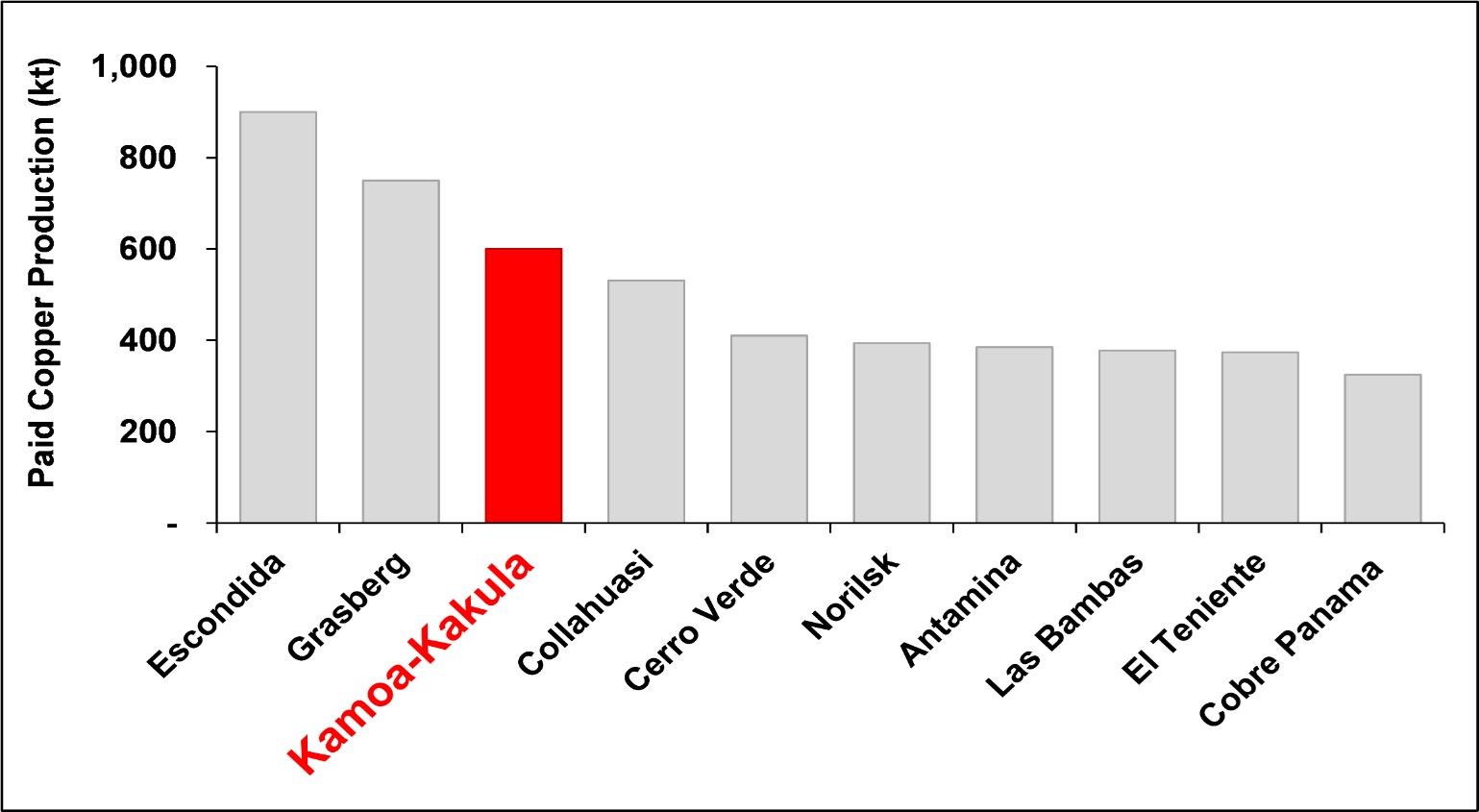

Figure 1: Kamoa-Kakula's base-case, pro-forma Phase 3 copper production (after de-bottlenecking of Phase 1 and 2 is complete) relative to the world's projected top 10 producing mines in 2022 by payable copper production.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_008full.jpg

Source: company filings, Wood Mackenzie (April 2022). Note: Kamoa-Kakula production of 600 kt copper in concentrate is based on expected Phase 1, 2 and 3 steady state production, following de-bottlenecking of both Phase 1 and 2 concentrators, and commercial ramp-up of the Phase 3 concentrator.

Figure 2: Kamoa-Kakula's Phase 1, Phase 2 and Phase 3 mine, processing plants and infrastructure layout.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_009full.jpg

Phase 3 basic engineering nearing completion, procurement activities have commenced

Basic engineering design for the Phase 3, 5-million-tonne-per-annum concentrator plant, smelter and associated infrastructure is nearing completion. Procurement activities have commenced with the following long-lead order items placed in June: ball mills, concentrate filters, cone crushers and flotation cells. The earthworks contract has also recently been placed. The associated power and surface infrastructure for Phase 3 will be designed to support future expansions.

Following the commissioning of Phase 3, expected by the end of 2024, Kamoa-Kakula will have a total processing capacity of more than 14 million tonnes per annum. The completion of Phase 3 is expected to increase copper production capacity to approximately 600,000 tonnes per annum. This production rate will position Kamoa-Kakula as the world's third-largest copper mining complex, and the largest on the African continent.

Phase 3 boxcut for the new Kamoa 1 and Kamoa 2 underground mines nearing completion, excavation of the twin declines advancing rapidly

Construction is nearing completion on the Phase 3 box cut and decline ramp at the Kamoa 1 and Kamoa 2 mines, while excavation of the twin declines to access Phase 3 mining areas also is advancing well. Construction works for the ramp, cut-off drains, and water-collection sumps are well advanced.

Construction progress on the new twin declines is advancing rapidly at the Kamoa 1 and Kamoa 2 mines.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_010full.jpg

Machine operator Serge Muteba at work on a new tunnel connection at the Kamoa 1 and Kamoa 2 twin declines.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_011full.jpg

Basic engineering complete and initial long-lead equipment ordered for Kamoa-Kakula's direct-to-blister flash smelter

Kamoa-Kakula's Phase 3 expansion includes a 500,000-tonne-per-annum, direct-to-blister flash smelter to produce approximately 99% copper metal, and the replacement of Turbine #5 at the Inga II hydroelectric power station. The turbine replacement will supply an additional 178-megawatts (MW) of clean hydroelectric power to the national grid.

Earthworks excavation at the smelter site is progressing well, adjacent to Kamoa-Kakula's Phase 1 and Phase 2 concentrator plants, with bush clearing and top-soil stripping well advanced.

In June, purchase orders were placed for the smelter's slag cleaning furnace, anode refining furnaces and electrostatic precipitators, while basic engineering on the smelter design has been completed.

The Kamoa-Kakula smelter uses technology supplied by Metso Outotec of Espoo, Finland, and meets the International Finance Corporation's (IFC) emissions standards. The smelter has been sized to process most of the copper concentrate forecast to be produced by Kamoa-Kakula's Phase 1, Phase 2, and Phase 3 concentrators.

Phase 3 and the smelter will be powered by hydroelectricity generated from the 178-MW Inga II hydro facility, which is currently undergoing refurbishment, at a cost of approximately 6 cents per kilowatt hour.

Smelter civil works (as part of the earthworks package), including the erection of concrete retaining walls, now are well underway.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_012full.jpg

Geotechnical drilling is underway in preparation of construction of the main structure for Kamoa-Kakula's direct-to-blister flash smelter.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_013full.jpg

Draw-down of surface ore stockpiles has commenced; stockpiles hold approximately 4.6 million tonnes grading 4.42% copper, containing more than 201,000 tonnes of copper

Kamoa-Kakula's total high- and medium-grade ore surface stockpiles totalled approximately 4.6 million tonnes at an estimated grade of 4.42% copper as of the end of June 2022. The operation mined 1.66 million tonnes of ore grading 5.51% copper in Q2 2022, which was comprised of 1.62 million tonnes grading 5.57% copper from the Kakula Mine, including 0.78 million tonnes grading 6.74% copper from the mine's high-grade centre.

Surface ore stockpiles contained more than 201,000 tonnes of copper as of the end of June 2022.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_014full.jpg

Kamoa-Kakula delivering Phase 1 and 2 copper concentrate and blister under off-take agreements

During the quarter, Kamoa Copper entered into an amendment to the existing off-take agreements for Phase 1 copper concentrate with CITIC Metal (HK) Limited (CITIC Metal) and Gold Mountains (H.K.) International Mining Company Limited, a subsidiary of Zijin, which includes the additional production volumes from Phase 2. The revised off-take agreements with CITIC Metal and Gold Mountains are evergreen for 50% each of the production volumes from Phase 1 and 2, and include both copper concentrate and blister copper resulting from processing of Kamoa-Kakula's copper concentrates at the nearby Lualaba Copper Smelter.

Kamoa Copper also recently entered into a third off-take agreement with Trafigura Pte. Ltd. (Trafigura) for a fixed volume of Kamoa-Kakula's concentrate production from 2022 to 2024, with such volume re-allocated on a pro-rata basis from CITIC Metal and Zijin.

Trafigura is one of the largest physical commodities trading groups in the world, and has significant experience in managing commodity logistics flows on the African continent.

All three off-takers are purchasing either the copper concentrate at the Kamoa-Kakula Mine or the blister copper at the Lualaba Copper Smelter on a free-carrier basis, meaning the buyers are responsible for arranging freight and shipment to the final destination, which is reimbursed on an open-book basis.

Kamoa Copper's concentrates and blister copper are exported via the ports of Durban in South Africa and Dar es Salaam in Tanzania, and to a lesser extent Walvis Bay in Namibia and Beira in Mozambique.

Inga II partnership to supply additional clean hydroelectric power for the Phase 3 expansion and smelter; EPC contract signed for Turbine #5 refurbishment

In July 2021, Ivanhoe Mines Energy DRC, a sister company of Kamoa Copper tasked with delivering reliable, clean, renewable hydropower to Kamoa-Kakula, signed an addendum of the financing agreement under a public-private partnership with the Democratic Republic of Congo's state-owned power company, La Société Nationale d'Electricité (SNEL), to upgrade a major turbine (#5) at the existing Inga II hydropower facility on the Congo River.

It was this same partnership that successfully refurbished the Mwadingusha hydropower plant in 2021, which now supplies approximately 78 MW of power into the Democratic Republic of Congo's national grid.

The Inga II project is expected to produce an additional 178 MW of renewable hydropower, providing Kamoa-Kakula and its associated smelter with sustainable electricity for Phase 3 and future expansions, while also benefitting local communities. The Inga II upgrade project is scheduled for completion in Q4 of 2024.

The work at Turbine #5 will include the upgrade and replacement of all the unit line from intake equipment, turbine, speed governor, alternator, voltage regulator and transformers (water to wire).

The Inga II Turbine #5 project has much lower unitary capital cost per megawatt produced ($0.58/MW) compared to the completed Mwadingusha project ($1.45/MW). The engineering, procurement, and construction (EPC) contract for the upgrading of Turbine #5 was signed in Heidenheim, Germany, on April 26, 2022, by SNEL and Voith Hydro, a leading German hydropower company.

Rehabilitation work under the private-public partnership now is underway to refurbish Turbine #5 at the Inga II hydropower facility.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_015full.jpg

Empowering local communities through sustainable development

Ivanhoe Mines founded the Sustainable Livelihoods Program in 2010 to strengthen food security and farming capacity in the host communities near Kamoa-Kakula. Today, approximately 900 community farmers are benefiting from the program, producing high-quality food for their families and selling the surplus for additional income. Sustainable Livelihoods commenced with maize and vegetable production, and now includes fruit, aquaculture, poultry and honey.

The banana plantation project began in 2018 and now consists of 11 hectares of banana trees. The 27 women from local communities who own this project harvested and sold more than 350 kilograms of bananas in July 2022.

Farmers from the local communities of Tshomeka, Katayi and Mundjendje harvesting bananas in July 2022.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_016full.jpg

Construction of additional livestock farming facilities is underway and planned to be completed in October. Together with the aquaculture project -comprised of approximately 140 fishponds with plans for the construction of another 100 new ponds - the livestock farm will significantly contribute toward local entrepreneurship and enhanced regional food security.

Construction of a health clinic at Muvunda Village has been completed and equipping of the facility is underway. Construction of a church at Tshilongo Village is approximately 60% complete. Kamoa-Kakula continued its support for the adult literacy training program, being implemented by a group of community participants who have been trained as facilitators.

Implementation of the first regulatory five-year community development plan, the Cahier des Charges, which provides $8.6 million towards educational, healthcare, agricultural, potable water provision, and other initiatives, is well underway. Construction of two early childhood development centres, planned for operation in September 2022, is nearing completion. The associated curriculum has been developed and is ready for implementation, thereby enabling access to these formative educational programs for the first time in the region. The Mupenda aquaculture project and the Muvunda poultry project also have been launched, and the planning and design of two rural community health centres has progressed well.

Local community enterprise programs continued, including the expansion of the brick-making and sewing facilities, as well as landscaping and gardening, which are under review seeking to enhance business efficiency and growth. An order has been placed for a new brick-making machine, which will see the production capacity double the average production to approximately 120,000 bricks per month. The extension of the sewing facility aims to double the current average monthly production rate of approximately 600 items of personal protective equipment.

Construction of a health clinic at the local community of Muvunda has been completed and equipping of the facility is underway.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_017full.jpg

| Kamoa-Kakula 2022 Guidance | ||

| Contained copper in concentrate | (tonnes) | 290,000 to 340,000 |

| Cash cost (C1) | ($ per pound) | 1.20 to 1.40 |

Copper Production and Cash Cost Guidance for 2022

The Kamoa-Kakula Phase 2, 3.8 million tonne per annum concentrator plant successfully declared commercial production on April 7, 2022. First ore was introduced into the Phase 2 milling circuit on March 21, 2022, with first copper concentrate produced approximately four months ahead of the originally announced development schedule. Management expects that with the early commissioning of the Phase 2 concentrator plant, Kamoa-Kakula will be able to deliver the upper end of its original 2022 copper production guidance of 290,000 to 340,000 tonnes. As a result, Ivanhoe Mines increases its 2022 production guidance range for Kamoa-Kakula to between 310,000 and 340,000 tonnes of copper in concentrate.

Kamoa-Kakula produced a total of 87,314 tonnes of copper in concentrate in Q2 2022, and 55,602 tonnes in the first quarter of 2022. The figures are on a 100% project basis and metal reported in concentrate is prior to refining losses, or deductions associated with smelter terms. Guidance involves estimates of known and unknown risks, uncertainties and other factors which may cause the actual results to be materially different.

Cash costs (C1) per pound of payable copper amounted to $1.42 for the second quarter of 2022, as compared to $1.21 and $1.28 in the first quarter of 2022 and the last quarter of 2021 respectively.

Cash costs for the second quarter included a significant increase in off-site concentrate transportation and logistics charges, which is projected to continue during the third quarter as a result of the ongoing maintenance at the Lualaba Copper Smelter and as Kamoa Copper and its partners implement logistical optimizations.

The previously announced cash cost (C1) per pound guidance for the 2022 financial year of $1.20 to $1.40 per pound remains unchanged. Cash cost is projected to come in at the upper end of the guidance range, subject to logistics costs easing in the fourth quarter.

Cash costs (C1) is a non-GAAP measure used by management to evaluate operating performance and includes all direct mining, processing, and general and administrative costs. Smelter charges and freight deductions on sales to final port of destination (typically China), which are recognized as a component of sales revenues, are added to C1 cash cost to arrive at an approximate cost of delivered finished metal.

For historical comparatives, see the Non-GAAP Financial Performance Measures section of this news release.

A breakdown of realized and provisionally priced copper production is as follows:

At the end of June 2022 there was an outstanding balance of 125,673 tonnes of provisionally priced copper in concentrate. Following the recent decline in the copper price, a remeasurement of $205 million was made to account for the change in copper price at period end.

| Q2 2022 | Q1 2022 | ||

| Realized payable copper (1) | (tonnes) | 50,642 | 53,056 |

| Realized copper price (1) | ($ per lb.) | 4.34 | 4.51 |

| New provisionally priced payable copper (2) | (tonnes) | 85,794 | 51,919 |

| Average price of new provisionally priced copper | ($ per lb.) | 4.32 | 4.54 |

| Copper price for remeasurement (mark-to-market) of provisional sales at period end | ($ per lb.) | 3.79 | 4.69 |

| Outstanding balance of provisionally priced payable copper (3) | (tonnes) | 125,673 | 90,544 |

Notes: (1) Payable copper that was provisionally priced in prior quarters and settled during the quarter. (2) Provisionally priced payable copper sold is subject to final pricing over the next several months. (3) Outstanding balance is made up of new provisionally priced payable copper from the current quarter, with the balance from the previous quarter.

2. Platreef Project

64%-owned by Ivanhoe Mines

South Africa

The Platreef Project is owned by Ivanplats (Pty) Ltd (Ivanplats), which is 64%-owned by Ivanhoe Mines. A 26% interest is held by Ivanplats' historically disadvantaged, broad-based, black economic empowerment (B-BBEE) partners, which include 20 local host communities with approximately 150,000 people, project employees and local entrepreneurs. A Japanese consortium of ITOCHU Corporation, Japan Oil, Gas and Metals National Corporation, and Japan Gas Corporation, owns a 10% interest in Ivanplats, which it acquired in two tranches for a total investment of $290 million.

The Platreef Project hosts an underground deposit of thick, platinum-group metals, nickel, copper and gold mineralization on the Northern Limb of the Bushveld Igneous Complex in Limpopo Province - approximately 280 kilometres northeast of Johannesburg and eight kilometres from the town of Mokopane.

On the Northern Limb, platinum-group metals mineralization is primarily hosted within the Platreef, a mineralized sequence traced for more than 30 kilometres along strike. Ivanhoe's Platreef Project, within the Platreef's southern sector, is comprised of two contiguous properties: Turfspruit and Macalacaskop. Turfspruit, the northernmost property, is contiguous with, and along strike from, Anglo Platinum's Mogalakwena group of mining operations and properties.

Since 2007, Ivanhoe has focused its exploration and development activities on defining and advancing the down-dip extension of its original discovery at Platreef, now known as the Flatreef Deposit, which is amenable to highly mechanized, underground mining methods. With Shaft 1, the initial access to the deposit, now in operation and hoisting development rock from underground, Ivanhoe is focusing on construction activities to bring Phase 1 of Platreef into production by Q3 2024.

Aerial view of the Platreef project showcasing latest construction activities, with Shaft 1 on the right, Shaft 2 hitch-to-collar construction on the left, and the radial stacker in the foreground.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_018full.jpg

Health and safety at Platreef

As at the end of June 2022, the Platreef Project reached 1,243,146 lost-time, injury-free hours worked.

Shaft 1 changeover to a production shaft completed, lateral underground mine development progressing well

Shaft equipping was successfully completed in March 2022, with Shaft 1 now fully commissioned for Phase 1 mining as planned. Following the completion of this changeover initial development started on the 950-metre level in April 2022.

Underground development work is focused on establishing the waste passes from the 750-metre and the 850-metre levels to the 950-metre level, installing the required underground infrastructure on the various stations, developing towards the first reef and stoping areas, as well as developing towards the first ventilation shaft location. Mine development on the 950-metre level progressed well with more than 200 metres of development successfully completed during the quarter. Mining on the 750-metre level and the 850-metre level will commence in Q3 and Q4 of 2022.

Ivanplats' initial order with Epiroc of Stockholm, Sweden, for its primary mining fleet includes emissions-free, battery-electric jumbo face drill rigs, 14-tonne battery-electric scooptrams, battery-electric bolting rigs and 42-tonne battery-electric dump trucks. The first ordered fleet has been delivered, slung down and are progressing with lateral underground development.

Construction of Platreef's first solar-power plant is scheduled to commence in Q3 2022, with commissioning expected in 2023. The solar-generated power from the plant will be used for mine development and construction activities, as well as for charging Platreef's battery-powered underground mining fleet.

A battery electric ST14 Scooptram from Epiroc operating underground at Platreef. Mine development on the 950-metre-level progressed well in Q2 2022.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_019full.jpg

Shaft 2 headgear construction from hitch to collar successfully completed

The 10m diameter Shaft 2, which will be the among the largest hoisting shafts on the African continent, is on the critical path for the future Phase 2 expansion of Platreef. Following the completion of the 26m concrete hitch to collar construction in August 2022, Ivanplats plans to continue with the construction of the 103-metre-tall concrete headgear (headframe) which will house the shaft's permanent personnel and rock hoisting facilities. The pilot drilling required for the raise bore center hole of the shaft and the commencement of the sliding of the headframe are both planned to commence before the end of 2022. This will allow for optionality in bringing forward the timeline of Phase 2 production.

Shaft 2 headgear construction from hitch to collar (in red circle) now is complete.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_ivan25en.png

Outstanding results of Platreef 2022 Feasibility Study

On February 28, 2022, Ivanhoe Mines announced the results of a new independent feasibility study for the Platreef Project (Platreef 2022 FS). The Platreef 2022 FS is based on a two-phased development to a steady-state production rate of 5.2 million tonnes per annum, and is the current execution plan for the Platreef Project.

Highlights of the Platreef 2022 FS include:

Figure 3: Production and timeline schematic from the Platreef 2022 Feasibility Study.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_022full.jpg

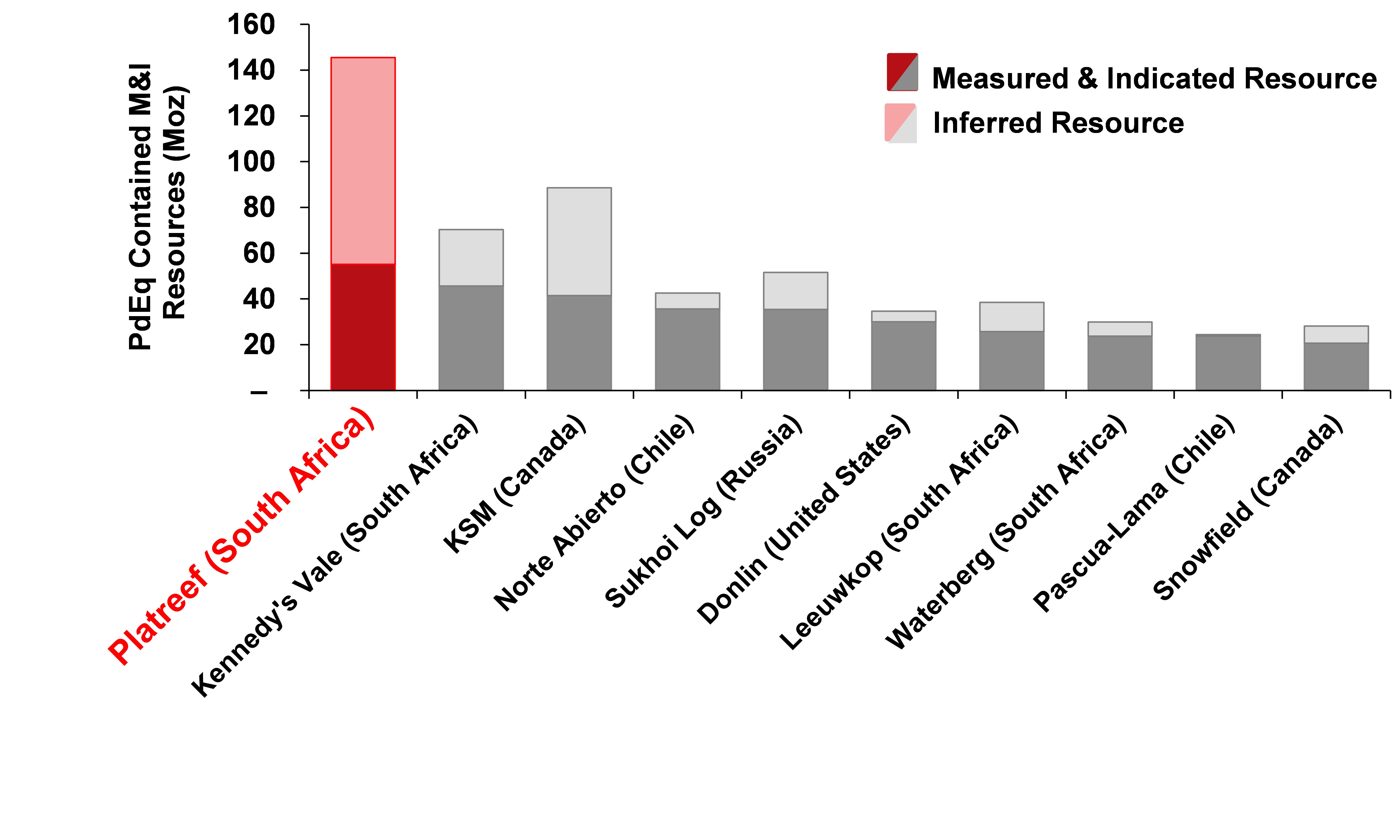

Figure 4: World's largest precious metal deposits under development ranked by contained metal in Measured and Indicated Resources.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_023full.jpg

Source: company filings, S&P Global Market Intelligence. Notes: Chart ranks the largest undeveloped primary palladium, platinum, gold, silver and rhodium projects from the S&P Global Market Intelligence database based on measured and indicated palladium equivalent resource. Palladium equivalent calculation includes palladium, platinum, gold, silver and rhodium ounces and has been calculated using spot price metal price assumptions (February 23, 2022) of US$1,095/oz. platinum, US$2,480/oz. palladium, US$18,750/oz. rhodium, US$1,909/oz. gold and US$24.55/oz. silver. Measured and Indicated resources for Platreef correspond to palladium, platinum, gold and rhodium ounces at a 1 g/t cut-off grade.

Platreef development currently funded by $300-million stream financing with efforts to finalize additional senior debt facility well underway

In December 2021, Ivanplats entered a gold, palladium and platinum stream financing with Orion Mine Finance, a leading international provider of customized financing to mining companies, and Nomad Royalty Company, a precious metals royalty company, in which Orion Mine Finance is a significant shareholder (Orion Mine Finance and Nomad Royalty Company, together, the Stream Purchasers). Ivanplat's current Phase 1 development costs are being funded by the first prepayment of $75 million received in December 2021 following the closing of the transaction, with a further $225 million expected to be paid upon satisfaction of certain conditions precedent during the Q3 2022. Both the gold stream facility, and palladium and platinum stream facility, will be subordinated to any senior secured financing.

The senior debt facility of up to $150 million is anticipated to be used only after the stream facilities are fully drawn. Ivanplats remains flexible to raise additional debt or equity later, and has pre-agreed with the Stream Purchasers the inter-creditor arrangements for any future senior debt. While the stream facilities are guaranteed by Ivanplats and secured over the assets and Ivanhoe's shares of Platreef, there is no recourse to Ivanhoe Mines.

Supply of bulk power to Platreef (100 MVA)

Final agreements for the 100 megavolt-amperes (MVA) power supply from Eskom, the South African public electricity utility, were signed during Q2 2022 and the construction permit was received. Construction of the overhead line has commenced, and fabrication of the pylons is progressing. The bulk power project is scheduled for completion in Q4 2023.

Platreef continues focus on community development, human resources, and job training

Implementation of Platreef's second Social and Labour Plan (SLP) is underway. Ivanplats plans to build on the first SLP and continue with its training and development suite, including: 15 new mentorship initiatives; internal skills training for 78 staff members; a legends program to prepare retiring employees with new/other skills; community adult education training for host community members; core technical skills training for at least 100 community members; portable skills training, and more. Platreef also continues to support several educational programs and provide free Wi-Fi in host communities.

The first cadetship program, providing learnership opportunities to over 50 local students, was successfully completed. Selection is underway for the 50 beneficiaries of the second cadetship program, planned to commence in October 2022. Through this program, youth from the local community are afforded the opportunity to obtain a National Certificate in Health and Safety, as well as mining competencies, such as utility vehicle operations from the Murray & Roberts Training Academy. The cadetship program seeks to enhance gender diversity within the mine's workforce, targeting a minimum of 50% female representatives in the program. The first program successfully included 54% female students.

Local economic development projects will contribute to community water-source development through the Mogalakwena Municipality boreholes program. Activities undertaken include the tender process for the Ga-Magongoa community, as well as the launch of the social survey for the other five communities in preparation for the next phase of the water project. Other planned SLP projects, which will be conducted in partnership with other parties, include the refurbishment and equipping of a health clinic in Tshamahansi Village.

The enterprise-and-supplier development commitments comprise of expanding the existing kiosk and laundry facilities. New equipment has been installed at the laundry facilities, which increased capacity allows for service of the laundry needs of both the company and all on-site contractors. The planned kiosk expansion project will incorporate three separate facilities on site. The process of identifying local entrepreneurs to manage the kiosks is underway.

3. Kipushi Project

68%-owned by Ivanhoe Mines

Democratic Republic of Congo

The Kipushi zinc-copper-germanium-silver-lead mine in the DRC is adjacent to the town of Kipushi and approximately 30 kilometres southwest of Lubumbashi. It is located on the Central African Copperbelt, approximately 250 kilometres southeast of the Kamoa-Kakula Mining Complex and less than one kilometre from the Zambian border. Ivanhoe acquired its 68% interest in the Kipushi Project in November 2011, through Kipushi Holding that is 100%-owned by Ivanhoe Mines. The balance of 32% in the Kipushi Project is held by the state-owned mining company, Gécamines.

Kipushi Holding and Gécamines have signed a new agreement to return the ultra-high-grade Kipushi Mine back to commercial production. Kipushi will be the world's highest-grade major zinc mine, with an average grade of 36.4% zinc over the first five years of production.

Activities in 2022 to date includes the award of the mining contract for early works, repair of underground access roads required for future workings and recruitment of the key staff required for development.

In June 2022, Kipushi Holding together with Gécamines, approved the development budget for the Kipushi Project in line with the Kipushi 2022 Feasibility Study. Ordering of long-lead equipment is in process and early works construction activities now have commenced. Financing and offtake discussions are advancing with several interested parties.

Highlights of the new agreement include:

Health and safety at Kipushi

At the end of June 2022, the Kipushi Project reached 4,803,537 work hours free of lost-time injuries. It has been more than three and a half years since the last lost-time injury occurred at the project.

Community enrichment and development

The Kipushi Project has built a new potable water station to provide a free daily supply of water to the municipality of Kipushi. This daily supply to the Kipushi municipality community members includes power supply, disinfectant chemicals, routine maintenance, security and emergency repair of leaks to the primary reticulation to the benefit of an estimated 100,000 people. Approximately 1,000 cubic metres of potable water is pumped hourly and continuously to consumers on a daily basis.

50 boreholes of potable water are planned to be drilled around the Kipushi district over five years, to reach areas not served by current distribution. Four new water wells have been drilled, bringing the total to 16 solar-powered potable water wells, which have been installed by the Kipushi Project in the district.

The Kipushi Project continues to support educational initiatives through ongoing renovations at the Mungoti School, and the granting of bursaries and scholarships to students from Kipushi. A local orphanage was presented with a donation of books. Over 300 local beneficiaries are participating in an adult literacy and education program this year after the program resumed with physical classes following a two-year interruption due to the COVID-19 pandemic.

Kipushi feasibility study issued, heralding the planned re-start of the historic mine, with a two-year development timeline and exceptional economic results

On February 14, 2022, Ivanhoe Mines announced the positive findings of an independent, feasibility study for the planned resumption of commercial production at Kipushi.

The Kipushi 2022 Feasibility Study is based on a two-year construction timeline, which utilizes the significant existing surface and underground infrastructure to allow for substantially lower capital costs than comparable development projects. The estimated pre-production capital cost, including contingency, is $382 million.

The Kipushi 2022 Feasibility Study focuses on the mining of Kipushi's zinc-rich Big Zinc and Southern Zinc zones, with an estimated 11.8 million tonnes of Measured and Indicated Mineral Resources grading 35.3% zinc. Kipushi's exceptional zinc grade is more than twice that of the world's next-highest-grade zinc project, according to Wood Mackenzie, a leading, international industry research and consulting group (see Figure 5).

Figure 5: World's top 10 zinc projects, by contained zinc.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_024full.jpg

Source: Wood Mackenzie, January 2022. Note: All tonnes and metal grades of individual metals used in the equivalency calculation of the above-mentioned projects (except for Kipushi) are based on public disclosure and have been compiled by Wood Mackenzie. All metal grades have been converted by Wood Mackenzie to a zinc equivalent grade at Wood Mackenzie's respective long-term price assumptions.

The Kipushi 2022 Feasibility Study envisages the recommencement of underground mining operations, and the construction of a new concentrator facility on surface with annual processing capacity of 800,000 tonnes of ore, producing on average 240,000 tonnes of zinc contained in concentrate.

Highlights of the 2022 feasibility study results for the Kipushi Mine include:

The Kipushi 2022 Feasibility Study was independently prepared on a 100%-project basis by OreWin Pty. Ltd., MSA Group (Pty.) Ltd., SRK Consulting (Pty) Ltd. and METC Engineering.

Kipushi mining crews installing support bolts for cables and water pipes using a boom basket.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_025full.jpg

Recently upgraded underground mine with easy access to stopes allows for rapid production ramp-up

Mining at Kipushi historically has been carried out from the surface to a depth of approximately 1,220 metres. Shaft 5 (P5) is planned to be the main production shaft with a maximum hoisting capacity of 1.8 million tonnes per annum and provides the primary access to the lower levels of the mine, including the Big Zinc Zone, through the 1,150-metre haulage level.

Mining will be performed using highly productive, mechanized methods and cemented rock fill will be utilized to fill open stopes. Material generated underground will be trucked to the base of the P5 shaft, crushed and hoisted to surface. Personnel and equipment access also are via the P5 shaft. The Big Zinc Zone will be accessed by way of the existing decline, without significant new development required. As the existing decline already is below the first planned stoping level, it is relatively quick to develop the first zinc stopes for the ramp up of mine production.

Figure 6: Schematic section of Kipushi Mine. Shaft 5 (P5) is planned to be the main production shaft with a maximum hoisting capacity of 1.8 million tonnes per annum.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_026full.jpg

4. Western Foreland Exploration Project

90%- and 100%-owned by Ivanhoe Mines

Democratic Republic of Congo

Ivanhoe's DRC exploration group is targeting Kamoa-Kakula-style copper mineralization through a regional exploration and drilling program on its Western Foreland exploration licences, located to the north, south and west of the Kamoa-Kakula Project. Ivanhoe's Western Foreland Exploration Project consists of 17 licences that cover a combined area of approximately 2,407 square kilometres.

Exploration models that successfully led to the discoveries of Kakula, Kakula West, and the Kamoa North Bonanza Zone on the Kamoa Copper SA mining licence, are being applied to the Western Foreland extensive land package by the same team of exploration geologists responsible for the previous discoveries.

Exploration drilling in Q2 2022 was focused on additional drilling in the Makoko West area, drilling of stratigraphic holes in Lupemba area and regional stratigraphic sections on the permit north of the Kamoa-Kakula mining licence. A total of 39 diamond holes were completed during Q2 2022 to a total of 7,539 metres. In addition to the diamond drilling, 284 metres of air core drilling, within 8 holes, was completed at Makoko. Drilling expanded further afield during the period as the rainy season ended and the ground conditions improved.

The drilling of the Makoko West area is targeting the westerly extension of the Makoko Sud deposit discovered in 2018. Drilling is targeting shallow mineralization, less than 170 metres from surface, using Land Cruiser mounted rigs. In total, 2,802 metres in 21 holes were completed at Makoko West during Q2 2022.

A total of 1,716 metres of diamond drilling was completed in Q2 2022, in four holes, in the Mushiji permit, which is located approximately three kilometres north of the Kamoa-Kakula mining licence. Two five-kilometre-spaced drill fences were planned to test for the presence of lower Nguba and Roan Sandstone in the northern part of the permit. The drilling showed the northern section to have low prospectivity and no further work is planned. The southern portion of the licence still holds numerous prospective areas. A surface mapping program in the Mushiji area also was conducted to establish a more comprehensive surface geological map and assist with Roan distribution mapping.

Regional stratigraphic drilling during the quarter focused mainly on the Lupemba area in the far southwest of the Western Foreland licence package where the regional magnetic signature is more complex. In Q2 2022, diamond drilling for Lubudi, Kakula East and Lupemba were 890 metres, 1,025 metres and 1,106 metres, respectively.

Airborne gravity and electromagnetic helicopter surveys which began in 2021, recommenced and were nearly complete by the end of Q2 2022. Continued interpretation and processing of completed surveys is underway and will be used to better understand the structural domains and basin architecture over the Western Foreland. Ground gravity survey work is still in progress and will be used in conjunction with the airborne gravity to provide increased definition where required.

Ivanhoe's 2022 Western Foreland exploration expenditure is provisionally planned at $25 million. The main component of this expenditure is exploration drilling, with more than 50,000 metres of shallow (depth of less than 150 metres) air core, reverse circulation and diamond drilling focussed on defining sub-outcrop positions and obtaining bed-rock samples under the Kalahari sand cover. In addition, up to 45,000 metres of deeper regional drilling covering the entire 2,407 square kilometre land package is also provisionally planned, some of which is dependent upon exploration success.

Camp infrastructure upgrades during the quarter included the completion of the mobile phone tower construction and the associated IT infrastructure and high-speed internet connection.

SELECTED QUARTERLY FINANCIAL INFORMATION

The following table summarizes selected financial information for the prior eight quarters. Ivanhoe had no operating revenue in any financial reporting period. All revenue from commercial production at Kamoa-Kakula is recognized within the Kamoa Holding joint venture. Ivanhoe did not declare or pay any dividend or distribution in any financial reporting period.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_027full.jpg

DISCUSSION OF RESULTS OF OPERATIONS

Review of the three months ended June 30, 2022 vs. June 30, 2021

The company recorded a total comprehensive income of $340.9 million for Q2 2022 compared to a total comprehensive loss of $95.7 million for the same period in 2021. The profit for the period principally relates to the company's share of profit from the Kamoa Holding joint venture, the gain on fair valuation of embedded derivative liability and the recognition of the deferred tax asset relating to the Kipushi Project, all three of which are described in greater detail below.

Kamoa-Kakula sold 85,794 tonnes of payable copper in Q2 2022 realizing revenue of $494.1 million for the Kamoa Holding joint venture. Kamoa-Kakula's other operating data is summarized under the review of operations section. The company recognized income in the aggregate of $84.6 million from the joint venture in Q2 2022, which can be summarized as follows:

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_028full.jpg

The company's share of profit from the Kamoa Holding joint venture was $49.7 million in Q2 2022 compared to a loss of $10.0 million in Q2 2021. The following table summarizes the company's share of profit (loss) of the joint venture for the three months ended June 30, 2022, and for the same period in 2021:

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_029full.jpg

The company recognized a gain on fair valuation of the embedded derivative financial liability of $183.6 million for Q2 2022, compared to a loss on fair valuation of the embedded derivative financial liability of $85.7 million for Q2 2021.

Finance income for Q2 2022 amounted to $38.6 million and was $13.5 million more than for the same period in 2021 ($25.1 million). Included in finance income is the interest earned on loans to the Kamoa Holding joint venture to fund past development that amounted to $34.9 million for Q2 2022, and $23.0 million for the same period in 2021, and increased due to the higher accumulated loan balance.

With the agreement of the development plan by the shareholders of Kipushi and the approval of the development budget consistent with the Kipushi 2022 Feasibility Study, it now is deemed probable that future taxable profit will be available from the Kipushi Project, against which the unused tax losses and unused tax credits can be utilized. As a result, the company recognized the previously unrecognized deferred tax asset in June 2022, resulting in a deferred tax recovery (income) of $114.2 million.

Exploration and project evaluation expenditure amounted to $13.5 million in Q2 2022 and $12.0 million for the same period in 2021. Exploration and project evaluation expenditure related to exploration at Ivanhoe's Western Foreland exploration licences and amounts spent at the Kipushi Project, which was on reduced activities and incurred limited cost of a capital nature in the periods.

Review of the six months ended June 30, 2022, vs. June 30, 2021

The company recorded a total comprehensive income of $383.5 million for the six months ended June 30, 2022, compared to a loss of $79.5 million for the same period in 2021. The profit for the period principally relates to the company's share of profit from the Kamoa Holding joint venture, the gain on fair valuation of embedded derivative liability and the recognition of the deferred tax asset relating to the Kipushi Project, all three of which are described in greater detail below.

The Kamoa-Kakula Mining Complex sold 137,713 tonnes of payable copper in the six months ended June 30, 2022, realizing revenue of $1,013.7 million for the Kamoa Holding joint venture. Kamoa-Kakula's other operating data is summarized under the review of operations section. The company recognized income in aggregate of $200.0 million from the joint venture in the six months ended June 30, 2022, which can be summarized as follows:

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_030full.jpg

The company's share of profit from the Kamoa Holding joint venture was $136.8 million in the six months ended June 30, 2022, compared to a loss of $14.1 million in the same period in 2021. The following table summarizes the company's share of profit (loss) of the joint venture for the six months ended June 30, 2022, and for the same period in 2021:

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_031full.jpg

The company recognized a gain on fair valuation of the embedded derivative financial liability of $117.2 million for the six months ended June 30, 2022, compared to a loss on fair valuation of the embedded derivative financial liability of $60.1 million for the same period in 2021.

With the agreement of the development plan by the shareholders of Kipushi and the approval of the development budget consistent with the Kipushi 2022 Feasibility Study, it now is deemed probable that future taxable profit will be available from the Kipushi Project, against which the unused tax losses and unused tax credits can be utilized. As a result, the company recognized the previously unrecognized deferred tax asset in June 2022, resulting in a deferred tax recovery (income) of $112.8 million.

Finance income for the six months ended June 30, 2022, amounted to $70.1 million, and was $22.2 million more than for the same period in 2021 ($47.9 million). Included in finance income is the interest earned on loans to the Kamoa Holding joint venture to fund operations that amounted to $63.2 million for the six months ended June 30, 2022, and $44.1 million for the same period in 2021. Interest increased due to the higher accumulated loan balance.

Exploration and project evaluation expenditure amounted to $25.7 million in the six months ended June 30, 2022, and $20.7 million for the same period in 2021. Exploration and project evaluation expenditure related to exploration at Ivanhoe's Western Foreland exploration licences and amounts spent at the Kipushi Project, which was on reduced activities and incurred limited cost of a capital nature in the periods.

Financial position as at June 30, 2022, vs. December 31, 2021

The company's total assets increased by $291.8 million, from $3,218.2 million as at December 31, 2021, to $3,510.0 million as at June 30, 2022. The main reason for the increase in total assets was attributable to the increase in the company's investment in the Kamoa Holding joint venture by $200.0 million from $1,641.8 million as at December 31, 2021, to $1,841.8 million as at June 30, 2022.

The company's share of profit from the Kamoa Holding joint venture amounted to $136.8 million, while the interest on the loan to the joint venture amounted to $63.2 million for the six months ended June 30, 2022. The company's investment in the Kamoa Holding joint venture can be broken down as follows:

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_032full.jpg

Prior to commencing commercial production in July 2021, the Kamoa Holding joint venture principally used loans advanced to it by its shareholders to advance the Kamoa-Kakula Mining Complex through investing in development costs and other property, plant and equipment.

Going forward, all Phase 1 and Phase 2 operating costs and most Phase 3 capital expenditures are expected to be funded from copper sales and facilities in place at Kamoa-Kakula. Cash flows generated and used by the Kamoa Holding joint venture can be summarized as follows:

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_033full.jpg

The Kamoa Holding joint venture's net increase in property, plant and equipment from December 31, 2021, to June 30, 2022, amounted to $280.0 million and can be further broken down as follows:

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_034full.jpg

Ivanhoe's cash and cash equivalents decreased by $101.0 million, from $608.2 million as at December 31, 2021, to $507.2 million as at June 30, 2022. The company utilized $47.6 million of its cash in operating activities and spent $33.4 million acquiring property, plant and equipment. The company also invested $13.3 million in acquiring a strategic equity stake in Renergen Ltd., a South African emerging energy and helium producer.

The company's total liabilities decreased by $107.3 million to $733.9 million as at June 30, 2022, from $841.2 million as at December 31, 2021, with the decrease mainly due to the decrease in the embedded derivative liability linked to the convertible senior notes.

The net increase in property, plant and equipment amounted to $33.8 million, with additions of $41.2 million to project development and other property, plant and equipment. Of this total, $38.9 million pertained to development costs and other acquisitions of property, plant and equipment at the Platreef Project.

Costs incurred at the Platreef Project are deemed necessary to bring the project to commercial production and are therefore capitalized as property, plant and equipment.

Accounting for the convertible notes closed in March 2021

The company closed a private placement offering of $575.0 million of 2.50% convertible senior notes maturing in 2026 on March 17, 2021. Upon conversion, the convertible notes may be settled, at the company's election, in cash, common shares or a combination thereof. Due to this election right and conversion feature, the convertible notes have an embedded derivative liability that is measured at fair value with changes in value being recorded in profit or loss, as well as the host loan that is accounted for at amortized cost.

The convertible senior notes are senior unsecured obligations of the company which will accrue interest payable semi-annually in arrears at a rate of 2.50% per annum and will mature on April 15, 2026, unless earlier repurchased, redeemed or converted. The initial conversion rate of the notes is 134.5682 Class A common shares of the company per $1,000 principal amount of notes, or an initial conversion price of approximately $7.43 (equivalent to approximately C$9.31) per common share.

The effective interest rate of the host liability was deemed to be 9.39% and the interest recognized on the convertible notes amounted to $9.7 million in Q2 2022, after the capitalization of $0.7 million borrowing costs. The carrying value of the host liability was $450.9 million as at June 30, 2022, up from $437.4 million as at December 31, 2021.

The derivative liability had a fair value of $150.5 million on closure of the convertible notes offering and increased to $244.2 million as at December 31, 2021, and decreased to $127.0 million as at June 30, 2022, resulting in a gain on fair valuation of embedded derivative liability of $117.2 million for the six months ended June 30, 2022. The change in the fair value of the embedded derivative liability is largely due to the changes in the closing share price of the company's common shares at the different reporting dates.

The following key inputs and assumptions were used in determining the fair value of the embedded derivative liability:

| March 17, 2021 | March 31, 2021 | June 30, 2021 | Dec 31, 2021 | March 31, 2022 | June 30, 2022 | ||

| Share price | (C$/share) | C$7.00 | C$6.47 | C$8.95 | C$10.32 | C$11.66 | C$7.41 |

| Credit spread | (basis points) | 630 | 610 | 487 | 356 | 277 | 541 |

| Volatility | (%) | 42% | 42% | 40% | 40% | 40% | 40% |

| Borrowing cost | (basis points) | 50 | 50 | 50 | 25 | 25 | 25 |

| Fair value of derivative liability | ($'million) | $150.5 | $124.9 | $210.6 | $244.2 | $310.6 | $127.0 |

LIQUIDITY AND CAPITAL RESOURCES

The company had $507.1 million in cash and cash equivalents as at June 30, 2022. At this date, the company had consolidated working capital of approximately $529.5 million, compared to $654.8 million as at December 31, 2021.

The Platreef Project entered a gold, palladium and platinum stream financing in December 2021 that will fund a large portion of the Phase 1 capital costs. The stream facilities are a prepaid forward sale of refined metals, with prepayments totaling $300 million, available in two tranches with the first prepayment of $75 million received in December 2021 following the closing of the transaction and $225 million to be paid upon satisfaction of certain conditions precedent.

Kipushi Holding together with Gécamines, approved the development budget for the Kipushi Project in line with the Kipushi 2022 Feasibility Study. Ordering of long-lead equipment and other construction activities now have commenced. Financing and offtake discussions are advancing with several interested parties.

The company's main objectives for the remainder of 2022 at the Platreef Project are the continued development of the project towards the completion of its first phase currently scheduled for Q3 2024, as well as the continuation of the construction of the Shaft 2 headframe to allow optionality for possibly bringing Phase 2 forward. With the development plan and budget approved by Kipushi Holding together with Gécamines, Kipushi has commenced with the ordering of long-lead equipment and other construction activities as outlined in the 2022 feasibility study. With Phase 1 and Phase 2 commercial production achieved at the Kamoa-Kakula Mining Complex, the current focus is on operational efficiency and de-bottlenecking the Phase 1 and 2 operations, as well as progressing the Phase 3 expansion.

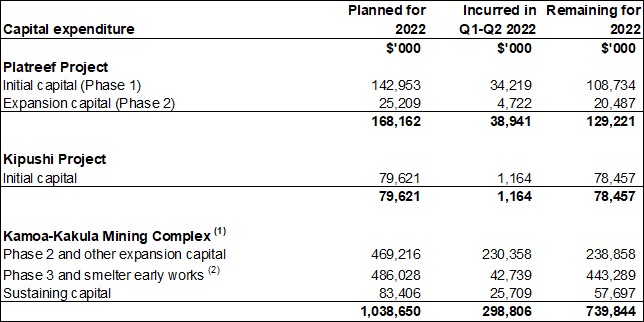

The company has forecast to spend $129 million on further development at the Platreef Project; $78 million on development at the Kipushi Project; and $21 million on corporate overheads for the remainder of 2022. Exploration activities at the Western Foreland exploration project in the DRC and other targets will continue in 2022 with an initial budget of $17 million for the remainder of 2022 on Western Forelands and $6 million on other targets. At the Kamoa Holding joint venture, all operating, and capital expansion costs are expected to be funded from copper sales and facilities in place at Kamoa.

The planned capital expenditure for 2022 can be broken down as follows:

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_035full.jpg

Notes: (1) Amounts in the above table for the Kamoa-Kakula Mining Complex are on a 100%-project basis. (2) The amount for Phase 3 and smelter early works is initial budgets only and will be augmented on completion of the updated pre-feasibility study.

On March 17, 2021, the company closed a private placement offering of $575 million of 2.50% convertible senior notes maturing in 2026. The convertible senior notes are senior unsecured obligations of the company which will accrue interest payable semi-annually in arrears at a rate of 2.50% per annum and will mature on April 15, 2026, unless earlier repurchased, redeemed or converted. The notes will be convertible at the option of holders, prior to the close of business on the business day immediately preceding October 15, 2025, only under certain circumstances and during certain periods, and thereafter, at any time until the close of business on the second scheduled trading day immediately preceding the maturity date. Upon conversion, the notes may be settled, at the company's election, in cash, common shares or a combination thereof. The carrying value of the host liability was $450.9 million and the fair value of the embedded derivative liability was $127.0 million as at June 30, 2022.

NON-GAAP FINANCIAL PERFORMANCE MEASURES

Kamoa-Kakula's C1 cash costs and C1 cash costs per pound

C1 cash costs and C1 cash costs per pound are non-GAAP financial measures. These are disclosed to enable investors to better understand the performance of Kamoa-Kakula in comparison to other copper producers who present results on a similar basis.

C1 cash costs are prepared on a basis consistent with the industry standard definitions by Wood Mackenzie cost guidelines but are not measures recognized under IFRS. In calculating the C1 cash cost, the costs are measured on the same basis as the company's share of profit from the Kamoa Holding joint venture that is contained in the financial statements. C1 cash costs are used by management to evaluate operating performance and include all direct mining, processing, and general and administrative costs. Smelter charges and freight deductions on sales to final port of destination, which are recognized as a component of sales revenues, are added to C1 cash cost to arrive at an approximate cost of finished metal. C1 cash costs and C1 cash costs per pound, exclude royalties and production taxes and non-routine charges as they are not direct production costs.

Reconciliation of Kamoa-Kakula's cost of sales to C1 cash costs, including on a per pound basis:

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_036full.jpg

All figures above are on a 100% basis.

EBITDA and EBITDA margin

EBITDA is a non-GAAP financial measure, which excludes income tax, finance costs, finance income and depreciation from net profit.

Ivanhoe believes that Kamoa-Kakula's EBITDA is a valuable indicator of the mine's ability to generate liquidity by producing operating cash flow to fund its working capital needs, service debt obligations, fund capital expenditures and distribute cash to its shareholders. EBITDA also is frequently used by investors and analysts for valuation purposes. EBITDA is intended to provide additional information to investors and analysts and does not have any standardized definition under IFRS and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. EBITDA excludes the impact of cash costs of financing activities and taxes, and the effects of changes in operating working capital balances, and therefore are not necessarily indicative of operating profit or cash flow from operations as determined under IFRS. Other companies may calculate EBITDA differently.

EBITDA margin is an indicator of Kamoa-Kakula's overall health and denotes its profitability, which is calculated by dividing EBITDA by revenue. EBITDA margin is intended to provide additional information to investors and analysts, does not have any standardized definition under IFRS, and should not be considered in isolation, or as a substitute, for measures of performance prepared in accordance with IFRS.

Reconciliation of profit (loss) after tax to EBITDA:

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/133832_f35aafe354d7a80b_037full.jpg

All figures above are for the Kamoa Holding joint venture on a 100% basis.

Qualified Persons

Disclosures of a scientific or technical nature at the Kamoa-Kakula Mining Complex in this news release have been reviewed and approved by Steve Amos, who is considered, by virtue of his education, experience and professional association, a Qualified Person under the terms of NI 43-101. Mr. Amos is not considered independent under NI 43-101 as he is the Head of the Kamoa-Kakula Mining Complex. Mr. Amos has verified the technical data disclosed in this news release.

Other disclosures of a scientific or technical nature regarding the stockpiles in this news release has been reviewed and approved by George Gilchrist, who is considered, by virtue of his education, experience and professional association, a Qualified Person under the terms of NI 43-101. Mr. Gilchrist is not considered independent under NI 43-101 as he is the Vice President, Resources of Ivanhoe Mines. Mr. Gilchrist has verified the other technical data disclosed in this news release.

Ivanhoe has prepared an independent, NI 43-101-compliant technical report for the Kamoa-Kakula Project, the Platreef Project and the Kipushi Project, each which is available on the company's website and under the company's SEDAR profile at www.sedar.com:

These technical reports include relevant information regarding the effective dates and the assumptions, parameters and methods of the mineral resource estimates on the Platreef Project, the Kipushi Project and the Kamoa-Kakula Mining Complex cited in this news release, as well as information regarding data verification, exploration procedures and other matters relevant to the scientific and technical disclosure contained in this news release in respect of the Platreef Project, Kipushi Project and Kamoa-Kakula Mining Complex.

About Ivanhoe Mines