Sudbury, Ontario--(Newsfile Corp. - January 31, 2022) - Magna Mining Inc (TSXV: NICU) (the "Company") is pleased to announce the results of the 2022 Feasibility Study for the Shakespeare Nickel Project ("Shakespeare") located 60 km south-west of Sudbury, Ontario. The Feasibility Study ("Study") is considered a base case and does not include any of the results from the 2021 Shakespeare drilling campaign (as highlighted in Figure 3). This Study remains within the constraints of current approvals, with only minor amendments and permits required prior to the start of construction. Shakespeare has a filed Closure Plan that has been accepted (approved) by the Ministry of Northern Development, Mines, Natural Resources and Forestry, and has obtained major permits for construction of a 4500 tonne per day (tpd) open pit mine, mill and tailing storage facility.

Included in the feasibility study is an analysis of the greenhouse gas (GHG) emissions over the life-of-mine. The deposit type, availability of renewable energy and emission reduction opportunities will allow the Shakespeare site to extract ore and produce nickel and copper concentrates with below average emission intensity. Verified carbon offsets for the remaining GHG emission sources have been included in operational costs, resulting in a carbon neutral nickel mining operation.

Highlights Include (all results are reported in Canadian Dollars unless otherwise noted):

- Base Case results demonstrate a Pre-Tax NPV6% of $221 million, IRR of 27.2%, and a 3.4-year payback, and a Post-Tax NPV6% of $140 million, IRR of 21.5% and 3.5 year post-tax payback period based on metal prices of US$ 8.50/lb. nickel, US$ 3.95/lb. copper, US$ 24/lb. cobalt, US$ 950/oz platinum, US$ 1,750/oz palladium and US$ 1,600 gold and an exchange rate of 0.77 US$:CDN.

- Initial capital requirements of $232.9 million, including all mine pre-production costs, co-disposal area preparation and sustaining capital of $9.2 million (including closure).

- Operating Costs of $41.18/t ore include carbon offset purchases

- Cash cost of US$(-0.76)/lb. nickel and AISC of US$(-0.61)/lb. nickel net of copper, cobalt and PGM by-product credits

- Recovered in concentrate nickel of 65.7 million pounds, copper of 86.7 million pounds, cobalt of 3.0 million pounds and PGM's of 177,000 ounces

- Average strip ratio of 4.98:1 with 11.9 million tonnes of reserves

Magna Mining CEO Jason Jessup commented: "This feasibility study demonstrates why we think the Shakespeare Nickel Project has the potential to be the next nickel producing project in Canada, and it confirms our belief that Shakespeare is an attractive stand-alone operation at current nickel and copper prices. The results of the study show positive economics, a modest upfront capital cost and strong leverage to the price of nickel and copper. Building the project as outlined in the feasibility would also give us a cornerstone asset with which to pursue Magna's vision of developing a hub and spoke production model in the world class Sudbury nickel mining camp. Aside from organic growth at our Shakespeare Project, we are evaluating acquisition opportunities that have synergies with Shakespeare. We are quite proud that the Study also includes detailed carbon accounting and incorporates the purchase of carbon offset credits to become a carbon neutral nickel mining operation. We believe that Shakespeare is the only feasibility stage nickel project in North America that can make this claim."

Paul Fowler, Magna Mining SVP added: "We are delighted to be able to complete this feasibility study within a year of our 2021 public listing, and it demonstrates the potential for Shakespeare to be Canada's next producing nickel mine. Our recent successful drill campaigns at the Shakespeare Mine and the adjacent P-4 exploration target also provide encouraging evidence that we will be able to fulfill our goal of further growing the resources at Shakespeare, potentially extending the life of mine and making new discoveries on our property package."

Financial Analysis

The Base Case using US$8.50/lb. nickel, US$3.95/lb. copper, US$ 24/lb. cobalt, US$ 950/oz platinum, US$ 1,750/oz palladium and US$ 1,600 gold and an exchange rate of 0.77 US$:CDN generates a before tax NPV6% of $221 million and an IRR of 27.2%, with a 3.4 year payback. After-tax NPV6% is $140 million, with an Internal Rate of Return (IRR) of 21.5%. Payback on the initial capital is 3.5 years.

Table 1: Summary of Shakespeare Project Economic Results - Metal Price Sensitivity

| Units | Upside Case | Spot Price Jan 2022 | Base Case | Low Case | |

| Nickel | US$/lb. | 12.00 | 10.28 | 8.50 | 7.00 |

| Copper | US$/lb. | 4.75 | 4.44 | 3.95 | 3.00 |

| Cobalt | US$/lb. | 33.00 | 32.66 | 24.00 | 17.50 |

| Platinum | US$/oz | 1,000 | 1,030 | 950 | 900 |

| Palladium | US$/oz | 2,150 | 2,153 | 1,750 | 1,400 |

| Gold | US$/oz | 1,850 | 1,838 | 1,600 | 1,500 |

| Pre-Tax NPV (6%) | CDN$ millions | 487 | 380 | 221 | 43 |

| Pre-Tax IRR | % | 51.1 | 41.5 | 27.2 | 10.3 |

| Post-Tax NPV (6%) | CDN$ millions | 318 | 247 | 140 | 14 |

| Post-Tax IRR (%) | % | 41.1 | 33.3 | 21.5 | 7.5 |

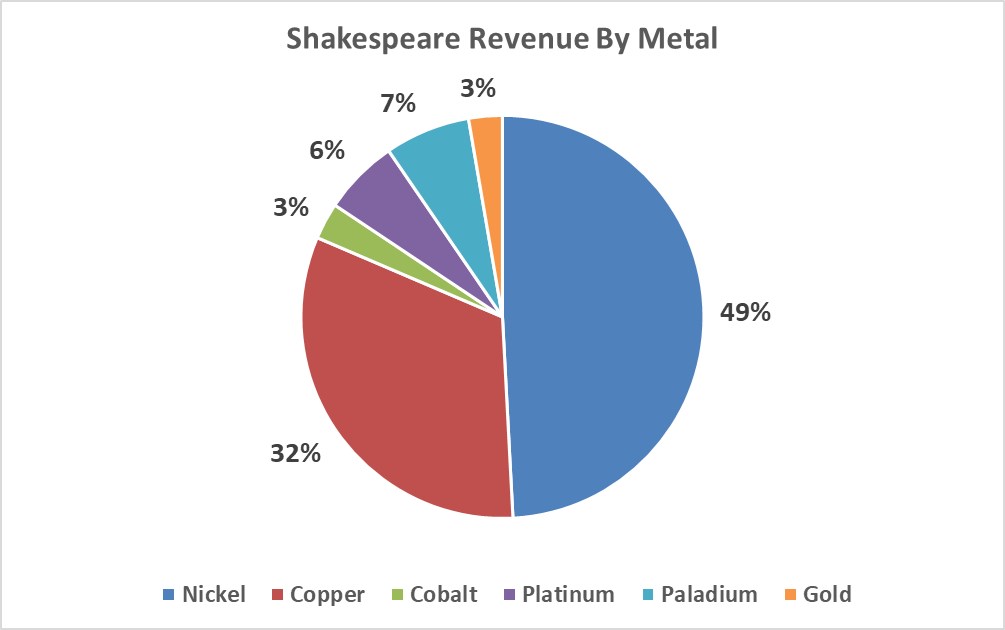

Revenue for the project is primarily from nickel (49%) with copper as the second largest revenue contributor (32%). Cobalt and PGM's account for the remainder of revenues as shown in Figure 1.

The Study has a mine life of 7.1 years with the current reserves.

Figure 1: Shakespeare Revenue By Metal

To view an enhanced version of Figure 1, please visit:

https://orders.newsfilecorp.com/files/8002/112113_d8db3eb98476a8be_002full.jpg

Capital and Operating Costs

The Study was prepared in accordance with National Instrument 43-101 (NI 43-101 of the Canadian Securities Administrators). The capital and operating cost estimates are summarized below. The operating costs have been detailed in Table 2, cash costs in Table 3 and the capital costs in Table 4.

The operating costs are estimated at $41.18/t ore over the mine life which include the purchase of carbon offsets and financing of the mining fleet with a 20% initial payment. The initial capital cost is $232.9 million with sustaining capital of $9.2 million including closure. The All In Sustaining Cost (AISC) is US$(0.61)/lb. nickel payable, net of by-product credits.

Table 2: Operating Cost Summary (CDN$)

| Operating Cost | Cost ($ M) | $/t Ore |

| Mining | 243.7 | 20.53 |

| Processing | 179.7 | 15.14 |

| G&A | 35.3 | 2.98 |

| Transport & Refining | 9.2 | 0.78 |

| Carbon Offset Purchase | 3.1 | 0.26 |

| Royalties | 17.7 | 1.49 |

| Total Operating Cost | 488.8 | 41.18 |

Table 3: Cash Costs and All In Sustaining Costs (US$)

| Operating Cost | Units | Cost |

| Nickel Cash Cost | US$/lb. payable | $8.00 |

| Nickel Cash Cost (including by-product credits) | US$/lb. payable | $ (0.76) |

| Nickel All In Sustaining Costs (AISC) | US$/lb. payable | $8.15 |

| Nickel AISC (including by-product credits) | US$/lb. payable | $(0.61) |

Table 4: Capital Cost Summary ($CDN)

| Capital Cost | Total ($ M) | Initial ($M) | Sustaining ($M) |

| Mining | 61.4 | 58.7 | 2.6 |

| Processing | 64.8 | 63.5 | 1.3 |

| Infrastructure | 59.3 | 59.3 | - |

| Environmental | 7.0 | 1.8 | 5.2 |

| Subtotal | 192.5 | 183.4 | 9.1 |

| Indirects | 29.9 | 29.9 | - |

| Contingency | 19.7 | 19.6 | 0.1 |

| Total Capital Cost | 242.1 | 232.9 | 9.2 |

The Study estimates the metal production as shown in Table 5.

Table 5: Life of Mine Metal Production

| Metal | Recovery (%) | Contained Metal in Concentrate (Mlbs. or K oz) |

| Nickel | 76.8 | 65.7 |

| Copper | 95.1 | 86.7 |

| Cobalt | 55.9 | 3.0 |

| Platinum | 76.2 | 93 |

| Palladium | 42.9 | 58 |

| Gold | 38.3 | 26 |

Mining and Infrastructure

The Study considers the use of an owner operated fleet including 12-91 tonne trucks, hydraulic excavators, wheel loaders and drills. The mine is designed to provide 4,500 tpd of mill feed to the process plant to be constructed adjacent to the pit. The annual mining rate averages 11.5 Mtpa in the first four years, peaking at 11.9 Mtpa in Year 3 before tapering off until the end of the mine life. The production profile is shown in Figure 2 with the two main grade items: nickel and copper.

Figure 2: Shakespeare Mine Production Profile

To view an enhanced version of Figure 2, please visit:

https://orders.newsfilecorp.com/files/8002/112113_d8db3eb98476a8be_003full.jpg

Material from the pit will be used to construct the Co-Disposal Area (CDA) for storage of waste and tailings in the adjacent valley. This facility will be lined allowing the long-term storage of potentially acid generating tailings (PAG) material from the process plant and any PAG material from the mine beneath the water level and control of the drainage from the waste stored within its footprint. The process plant will generate both PAG tailings and non-acid generating tailings (NAG) that are separated at the plant. The NAG tailings will be stored with the NAG waste rock from the mine. NAG waste not used in construction of the plant pad and haul roads will be stored in the CDA. The CDA includes a settling pond, polishing pond and water treatment facility for any variances in water quality encountered prior to discharge to the environment. The water management system has been designed to reuse site water for process applications, minimize freshwater requirements and effectively collect contact run-off in accordance with legislative requirements.

The Shakespeare benefits from past mining infrastructure that still exists and its proximity to Sudbury. This enables the mine to operate without the need of camp facilities due to its all-season road currently in place. Existing infrastructure and nearby infrastructure include:

- All season access road only requiring minor upgrading

- Existing sand and gravel quarries for construction material of the plant and CDA

- Access to hydro power at Espanola for quick connection to the grid

- Settling ponds in place adjacent to the pit

- Access to the edges of the pit for mining equipment

Mineral Resources and Reserves

The Open Pit Indicated Mineral Resource Estimate upon which the Study is based includes 203.8 Mlbs of nickel equivalent from 16.51 Mt grading 0.34% nickel, 0.36% copper, 0.02% cobalt, 0.33 g/t platinum, 0.36 g/t palladium and 0.19 g/t gold. No Inferred Mineral Resource is contained within the Mineral Resource pit shell.

Underground Mineral Resources use a 0.4% NiEq cutoff and are estimated below the open pit resource shell. The Underground Mineral Resource contains 44.8 Mlbs of nickel equivalent Indicated Resource and 29.6 Mlbs of nickel equivalent in the Inferred Resource.

The mineral resources are shown in Table 6.

Table 6: Shakespeare Mineral Resources (June 1, 2021)

| Units | Open Pit | Underground | Total | |||||

| Indicated | Indicated | Inferred | Indicated | Inferred | ||||

| Cutoff | Ni Eq% | 0.2% | 0.4% | 0.4% | 0.2/0.4% | 0.4% | ||

| Tonnage | M Tonnes | 16.51 | 3.83 | 2.36 | 20.34 | 2.36 | ||

| Nickel | % | 0.34 | 0.31 | 0.33 | 0.33 | 0.33 | ||

| Copper | % | 0.36 | 0.36 | 0.40 | 0.36 | 0.40 | ||

| Cobalt | % | 0.02 | 0.02 | 0.02 | 0.02 | 0.02 | ||

| Platinum | g/t | 0.33 | 0.30 | 0.34 | 0.32 | 0.34 | ||

| Palladium | g/t | 0.36 | 0.32 | 0.37 | 0.35 | 0.37 | ||

| Gold | g/t | 0.19 | 0.19 | 0.20 | 0.19 | 0.20 | ||

| Nickel Equivalent | % | 0.56 | 0.53 | 0.57 | 0.55 | 0.57 | ||

| Nickel | Mlbs. | 123.7 | 26.2 | 17.1 | 149.9 | 17.1 | ||

| Copper | Mlbs. | 131.0 | 30.4 | 20.8 | 161.4 | 20.8 | ||

| Cobalt | Mlbs. | 7.3 | 1.7 | 1.0 | 9.0 | 1.0 | ||

| Platinum | K oz | 175.1 | 25.3 | 17.7 | 200.5 | 17.7 | ||

| Palladium | K oz | 191.1 | 27.0 | 19.2 | 218.1 | 19.2 | ||

| Gold | K oz | 100.8 | 16.1 | 10.4 | 116.9 | 10.4 | ||

| Nickel Equivalent | Mlbs. | 203.8 | 44.8 | 29.6 | 248.6 | 29.6 | ||

- Mineral Resources are exclusive of material mined.

- CIM (2014) definitions were followed for Mineral Resources Reporting.

- Mineral resources which are not mineral reserves do not have demonstrated economic viability. All figures are rounded to reflect the relative accuracy of the estimate. Composites have been capped where appropriate.

- Open pit Mineral Resources are reported at a base case cut-off grade of 0.2% NiEq within a conceptual pit shell.

- Underground (below-pit) Mineral Resources are estimated from the bottom of the pit and are reported at a base case cut-off grade of 0.4% NiEq. The underground Mineral Resource grade blocks were quantified above the base case cut-off grade, below the constraining pit shell and within the constraining mineralized wireframes. At this base case cut-off grade the deposit shows excellent deposit continuity.

- Based on the size, shape, and orientation of the Deposit, it is envisioned that the underground mineralization may be mined using the longitudinal longhole retreat mining method (a branch of the generic mining method known as sublevel stoping).

- A fixed specific gravity value of 3.00 was used to estimate the resource tonnage from block model volumes; an SG of 2.85 for waste.

- NiEq Cut-off grades are based on metal prices of $7.50/lb Ni, $3.25/lb Cu, $21.00/lb Co, $1,000/oz Pt, $2,000/oz Pd and $1,600/oz Au, and metal recoveries of 75% for Ni, 96% for copper, 56% for Co, 73% for Pt, 39% for Pd and 36% for Au.

- The results from the pit optimization are used solely for the purpose of testing the "reasonable prospects for economic extraction" by an open pit and do not represent an attempt to estimate mineral reserves. The results are used as a guide to assist in the preparation of a Mineral Resource statement and to select an appropriate resource reporting cut-off grade.

- The estimate of Mineral Resources may be materially affected by environmental, permitting, legal, title, taxation, socio-political, marketing, or other relevant issues. There is no certainty that all or any part of the Inferred Mineral Resource will be upgraded to an Indicated or Measured Mineral Resource as a result of continued exploration.

Mineral Reserves for the Shakespeare Project have been shown in Table 7. The Mineral Reserve is based on a marginal cutoff using a net smelter calculation which is equivalent to a 0.23% nickel cutoff grade.

Table 7: Shakespeare Mineral Reserves (December 31, 2021)

| Units | Open Pit | |

| Probable | ||

| Cutoff | Ni% | 0.23 |

| Tonnage | M Tonnes | 11.87 |

| Nickel | % | 0.33 |

| Copper | % | 0.35 |

| Cobalt | % | 0.02 |

| Platinum | g/t | 0.32 |

| Palladium | g/t | 0.36 |

| Gold | g/t | 0.18 |

| Nickel | Mlbs. | 85.6 |

| Copper | Mlbs. | 91.1 |

| Cobalt | Mlbs. | 5.4 |

| Platinum | K oz | 122.2 |

| Palladium | K oz | 135.7 |

| Gold | K oz | 68.9 |

Note: CIM Definition Standards (2014) were followed for calculating Mineral Reserves. The mineral reserve estimate is as of December 31, 2021 and is based on the mineral resource estimate for the Shakespeare Property dated June 1, 2021. The mineral reserve estimate was completed under the supervision of Gordon Zurowski, P.Eng. of AGP, who is a Qualified Person as defined under NI 43-101. Mineral reserves are stated within the final pit design based on metal prices of US$ 6.50/lb. nickel, US$ 3.00/lb. copper, US$ 17/lb. cobalt, US$ 900/oz platinum, US$ 1,700/oz palladium and US$ 1,500 gold and an exchange rate of 0.77 US$:CDN. Metal recoveries are 76.8% nickel, 95.1% copper, 55.9% cobalt, 76.2% platinum, 42.9% palladium and 38.3% gold. The nickel cutoff applied was 0.23% nickel. Open pit mining costs used were $2.30/t mined. Processing costs were $15.23/t ore and G&A was $2.59/t ore. Numbers may not sum due to rounding.

Opportunities for Optimization and Growth

Given that the feasibility study is based on maintaining the operational parameters under which permits for construction of the Shakespeare Mine, mill and tailings storage facility have been issued, numerous opportunities remain for optimization and growth. The most significant of these opportunities are:

- Expansion of Mineral Resources and Conversion to Mineral Reserves

- The feasibility study resources have an effective date of June 1, 2021 and therefore does not include the results of the 2021 drilling program at Shakespeare (with additional assays still pending). Reported assays in the Gap, West and East Zones will be incorporated into a resource update in the future (see Fig. 1).

- Underground Mining Potential

- Underground resources have been outlined beneath the Feasibility open pit which may represent an opportunity for low-cost, bulk underground mining. This will be investigated in future studies to determine if a viable underground mine could provide additional feed to the mill and extend the life of mine.

- Effect of Higher Nickel Prices on Final Pit Design

- Reserves for the Study were calculated using US$6.50/lb nickel, US$3.00/lb copper, US$17/lb cobalt, US$900/oz platinum, US$1700/oz palladium and US$1500/oz gold. At higher metal prices, there is potential to push the pit deeper which may incorporate additional resource material, possibly extending mine life.

- New Exploration Targets

- Magna intends to continue to explore and expand on existing mineralized targets which show potential to become economic, high grade satellite deposits to feed a future Shakespeare mill.

Figure 3: Longitudinal Section of Shakespeare Deposit Showing Feasibility Open Pit Design and Resource Shell and Selected Previously Reported 2021 Exploration Drilling Results

To view an enhanced version of Figure 3, please visit:

https://orders.newsfilecorp.com/files/8002/112113_d8db3eb98476a8be_004full.jpg

All composite intervals are reported as core length as true width has not been determined.

Nickel Equivalent (NiEq%) grade is calculated based on metal prices of $6.25/lb Ni, $2.80/lb Cu, $31.00/lb Co, $950/oz Pt, $900/oz Pd and $1,250.00/oz Au, and metal recoveries of 76.4% for Ni, 95.9% for Cu, 71% for Co, 74.8% for Pt, 42.4% for Pd and 38.4% for Au.

Qualified Person

Certain technical information in this press release has been reviewed and approved by Mynyr Hoxha, Ph.D., P.Geo., the Company's Vice President of Exploration. Dr. Hoxha is a qualified person under Canadian National Instrument 43-101. Dr. Hoxha is an employee of Magna and is not independent of the Company under NI 43-101

The Feasibility Study was prepared under the direction and supervision of Gordon Zurowski, P. Eng Principal Mining Engineer with AGP, and the supporting Technical Report (the "Technical Report") will be available on SEDAR (www.sedar.com) under the Company's issuer profile within 45 calendar days. Mr. Zurowski, who is an independent Qualified Person as defined under NI 43-101, has reviewed, and approved the technical information pertaining to the Feasibility Study disclosed in this press release.

About Magna Mining Inc.

Magna Mining is an exploration and development company focused on nickel, copper and PGM projects in the Sudbury Region of Ontario, Canada. The Company's flagship asset is the past producing Shakespeare Mine which has major permits for the construction of a 4500 tonne per day open pit mine, processing plant and tailings storage facility and is surrounded by a contiguous 180km2 prospective land package. Additional information about the Company is available on SEDAR (www.sedar.com) and on the Company's website (www.magnamining.com).

For further information, please contact:

Jason Jessup

Chief Executive Officer

or

Paul Fowler, CFA

Senior Vice President

Email: info@magnamining.com

Cautionary Statement

This press release contains certain forward-looking information or forward-looking statements as defined in applicable securities laws. Forward-looking statements are not historical facts and are subject to several risks and uncertainties beyond the Company's control, including statements regarding the production at the Shakespeare Mine, the economic and operational potential of the Shakespeare Mine, potential acquisitions, plans to complete exploration programs, potential mineralization, exploration results and statements regarding beliefs, plans, expectations, or intentions of the Company. Resource exploration and development is highly speculative, characterized by several significant risks, which even a combination of careful evaluation, experience and knowledge may not eliminate. All forward-looking statements herein are qualified by this cautionary statement. Accordingly, readers should not place undue reliance on forward-looking statements. The Company undertakes no obligation to update publicly or otherwise revise any forward-looking statements whether as a result of new information or future events or otherwise, except as may be required by law.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accept responsibility for the adequacy or accuracy of this press release.

![]()

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/112113

Source: Magna Mining Inc.