Want to curate the report according to your business needs

Report Description + Table of Content + Company Profiles

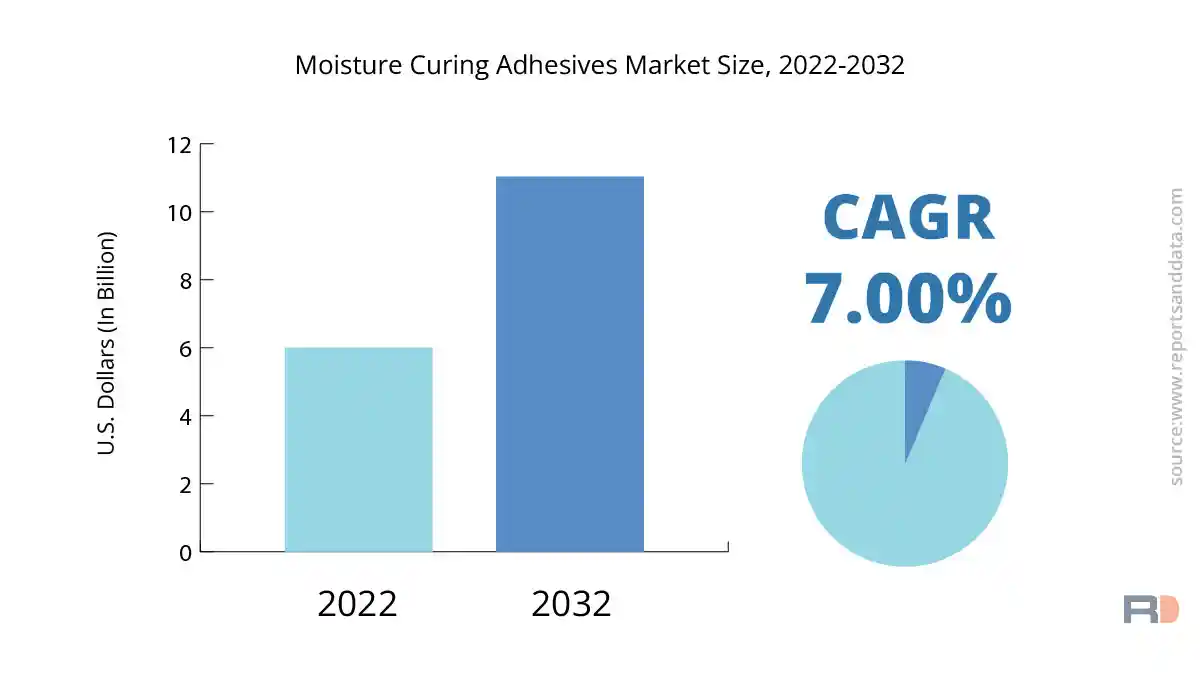

The global moisture curing adhesives market size was USD 6.0 billion in 2022 and is expected to reach USD 11.03 billion in 2032, and register a revenue CAGR of 7% during the forecast period. The demand for moisture-curing adhesives is on the rise across a variety of end-use industries, including the automotive, building, and woodworking sectors.

With their exceptional bonding strength and quick curing times, moisture-curing adhesives are frequently employed in the automotive sector. With their improved fuel economy and lower emissions, lightweight automobiles are becoming more popular, and these adhesives are employed in their manufacture. The demand for moisture-curing adhesives has also increased as a result of the growing usage of innovative materials in the automobile industry, such as Composites and Plastics. These adhesives are favored in the automobile industry because they can survive extreme environmental conditions and offer strong bonding between different components.

Moreover, a significant consumer of moisture-curing adhesives is the building industry. The capacity of these adhesives to join a range of substrates, including wood, metal, and Plastics, is raising demand for them in the construction sector. Flooring, insulation, and Roofing materials are frequently bonded together in the construction industry using moisture-curing adhesives. Also, the moisture curing adhesives market has grown as a result of the expanding trend of green construction techniques. These adhesives are safe for the environment and do not include any dangerous chemicals or Solvents.

In addition, a sizable portion of moisture-curing adhesives are used in the woodworking sector. In the woodworking business, these adhesives are used to join furniture, doors, windows, and other wooden structures. The capacity of moisture-curing adhesives to provide strong bonding, high water resistance, and quick curing time drives their demand in the woodworking sector. Also, the market for moisture-curing adhesives has grown as a result of the rising demand for high-end timber goods and custom-made furniture.

The growing emphasis on environmentally friendly and energy-efficient buildings also contributes to the need for moisture-curing adhesives. Regulations are being implemented by governments across the globe to promote the use of energy-efficient building materials. Moisture-curing adhesives are a great option for usage in environmentally friendly buildings because they emit less Volatile Organic Compounds (VOCs). Also, the growing need for energy-efficient structures has sparked the creation of sophisticated moisture-curing adhesives with improved insulating capabilities.

The short shelf life of these adhesives is one of the main obstacles. Adhesives that cure when exposed to moisture in the air are reactive materials. They, therefore, have a short shelf life and need to be properly preserved to avoid early curing. For producers and distributors, this can be difficult because it raises prices and limits the supply of certain adhesives.

The environmental and health risks linked to the usage of these adhesives are another factor restraining the moisture curing adhesives market revenue growth. Some moisture-curing adhesives contain isocyanates, which, if handled improperly, can be harmful to human health. In addition, using these adhesives can cause the release of Volatile Organic Compounds (VOCs), which can have a negative influence on the environment and contribute to air pollution.

The moisture curing adhesives market revenue growth is also constrained by the cost and availability of raw materials. These adhesives need the usage of specialized raw ingredients, such as silane-terminated polymers and Polyurethane prepolymers, which cannot always be accessible or can be subject to price changes. This can lead to a breakdown in the supply chain and higher production expenses, which can raise the price of these adhesives even more.

The market is additionally constrained by the moisture curing adhesives' poor performance in specific environments. The bonding strength and endurance of these adhesives can be impacted by their sensitivity to dampness and temperature. This can prevent them from being used in some situations, such as outdoor or hot environments.

The market for moisture-curing adhesives is dominated by the polyurethane category in 2023.

Based on type, the market for moisture-curing adhesives is divided into Polyurethane, Silicone, Cyanoacrylate, and Others. As a result of its high strength, longevity, and versatility, the polyurethane segment outpaces the others in the market. Construction, automotive, packing, among other industries, use polyurethane adhesives extensively. The market for polyurethane is expanding as a result of rising consumer demand for lightweight, fuel-efficient vehicles and the expanding construction sector. Also driving revenue growth in this market is anticipated to be the rising demand for polyurethane-based adhesives in packaging applications, such as food and Beverage Packaging.

Throughout the forecast period, the Silicone segment is anticipated to have the greatest revenue CAGR. Market expansion is being driven by the escalating demand for silicone-based adhesives in the healthcare sector, particularly in the manufacture of Medical Devices. Due to their biocompatibility and superior adhesion qualities, silicone-based adhesives are frequently used in medical devices such as Catheters, implants, and wound dressings, among others. The need for silicone-based adhesives in the healthcare sector is anticipated to increase further as the demand for minimally invasive procedures rises. Also, the electronics industry's expanding need for silicone-based adhesives, particularly in the production of smartphones and other electronic gadgets, is anticipated to fuel revenue growth in this sector.

Throughout the projection period, the cyanoacrylate segment is anticipated to experience moderate revenue growth. The automobile, electronics, and Medical Device sectors, among others, all employ cyanoacrylate adhesives extensively. Market expansion is being driven by the rising demand for cyanoacrylate-based adhesives in the automotive sector, particularly in the production of lightweight and fuel-efficient automobiles. In addition, the expanding need for cyanoacrylate-based adhesives in the electronics sector, particularly in the production of smartphones and other electronic devices, is anticipated to further fuel revenue growth in this market.

Epoxy, acrylic, and vinyl adhesives, among others, are included in the Others segment of the market. Throughout the projection period, this segment's revenue is anticipated to expand somewhat. Market expansion is being driven by the rising demand for epoxy-based adhesives in the construction sector, particularly in the production of composite materials. Moreover, the automotive industry's growing need for acrylic-based adhesives, particularly in the production of lightweight and fuel-efficient automobiles, is anticipated to further fuel revenue development in this sector.

In conclusion, the market for moisture-curing adhesives is anticipated to experience strong revenue growth during the projection period. Some factors driving the market's expansion include the rising need for minimally invasive operations, lightweight and fuel-efficient cars, and a booming construction sector. The Silicone sector is anticipated to grow at the highest revenue CAGR throughout the projected period, while the Polyurethane segment currently maintains a leading position in the market. Throughout the projection period, revenue growth is anticipated to be moderate in the Cyanoacrylate and Others categories.

Adhesives that cure when exposed to moisture in the air don't require any additional curing chemicals. They are known as moisture-curing adhesives. Due to these adhesives' excellent bonding abilities, longevity, and resilience to environmental elements including moisture, heat, and chemicals, they have become more and more common across a variety of industries. The automotive, construction, electronics, and other application categories make up the moisture curing adhesives market.

In terms of revenue, the construction industry led the moisture curing adhesives market in 2021. The necessity for high-performance bonding solutions in construction projects for buildings and infrastructure is the main factor driving the market for moisture curing adhesives. Moisture curing adhesives are frequently used for applications including Floor Coatings, waterproofing membranes, and structural bonding because they provide great adhesion to a variety of substrates, such as concrete, metal, glass, and plastics. The usage of moisture curing adhesives, which offer higher durability and resilience to external variables, has also increased as a result of the growing emphasis on ecological and energy-efficient construction methods. This decreases the need for routine maintenance and replacement

Throughout the forecast period, the automotive segment is anticipated to have the quickest revenue Growth. In the production of automobiles, moisture curing adhesives are frequently utilized for bonding tasks like windscreen installation, structural bonding, and interior trim attachment. These adhesives enhance the overall performance and efficiency of the vehicle by providing high-strength bonding, enhanced safety, and decreased weight. Also, the growing popularity of electric and Hybrid Vehicles, which call for bonding solutions that are lightweight and high-performing, is anticipated to fuel market expansion in the automotive sector.

Throughout the projection period, the electronics segment is also anticipated to have considerable expansion. In the production of electronics, moisture curing adhesives are frequently utilized for component glueing, sealing, and encapsulation. These adhesives provide exceptional protection for electronic equipment from moisture and the environment, extending their dependability and lifespan. Additionally, the market expansion in the electronics sector is anticipated to be fueled by the rising need for downsizing of electronic devices and components as well as the expanding Internet of Things (IoT) and smart device trends.

Throughout the anticipated period, the other application category, which includes sectors like packaging, healthcare, and aerospace, is also anticipated to expand steadily. Flexible Packaging, medical device assembly, and aerospace structural bonding are just a few of the many applications for which moisture curing adhesives provide high-performance bonding solutions.

In conclusion, the improved bonding capabilities, dependability, and resistance to environmental conditions offered by these adhesives are projected to propel the moisture curing adhesives market to experience considerable expansion across a variety of industries. While the automotive and electronics industries are anticipated to experience the highest growth during the projected period, the construction segment now holds the largest revenue share.

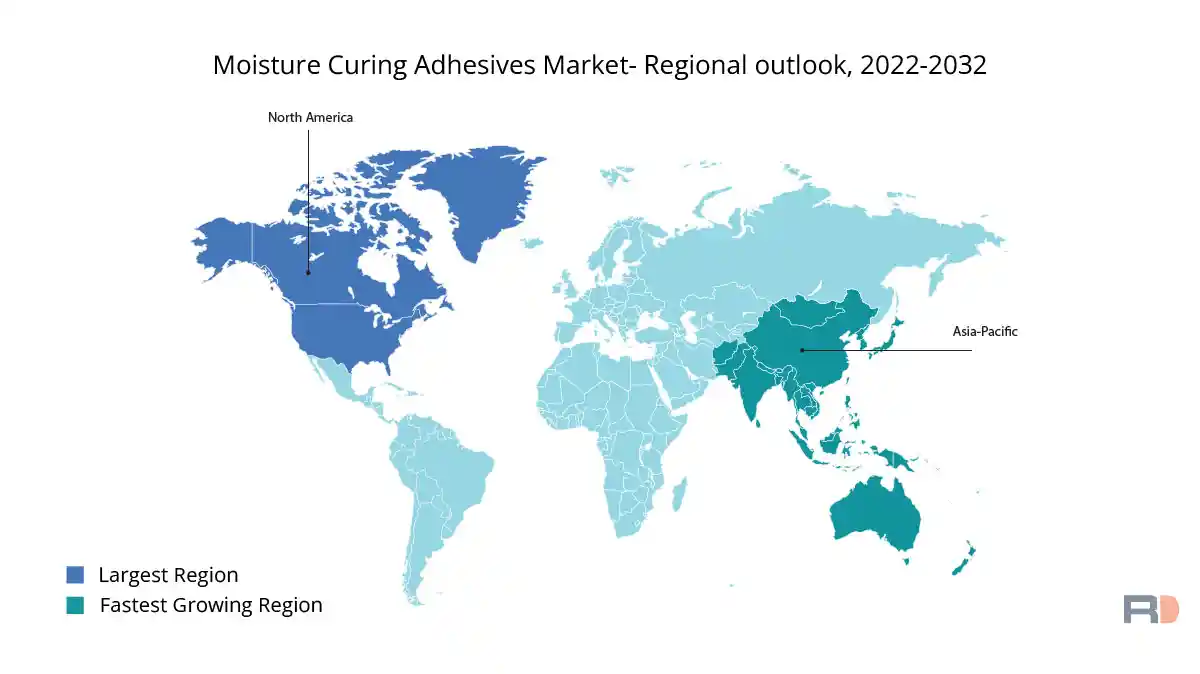

The North American, European, Asian Pacific, Middle East & Africa, and South American regions make up the various subregions of the worldwide moisture curing adhesives market. The development of the market for moisture-curing adhesives is influenced by a distinct set of factors in each location.

North America: Throughout the forecast period, North America is anticipated to account for a sizable portion of the global market for moisture-curing adhesives. The region's adhesives market is anticipated to increase as a result of the rising demand for adhesives across a number of end-use sectors, including electronics, automotive, and construction. Moreover, the existence of significant adhesive producers and the increased emphasis on R&D efforts are anticipated to support market expansion.

Europe: Throughout the projected period, Europe is anticipated to experience considerable expansion in the moisture curing adhesives market. One of the main end consumers of moisture-curing adhesives in the area is the well-established automotive industry. Additionally, it is anticipated that the region's market will rise faster due to the rising need for environmentally friendly and sustainable adhesives. Major auto and electronics firms' presence in the area is also anticipated to support market expansion.

Asia Pacific: Throughout the forecast period, Asia Pacific is anticipated to experience the moisture curing adhesives market's highest growth. The market in the region is anticipated to increase as a result of the rising demand for adhesives in sectors including electronics, construction, and the automotive industries. The region has become a significant manufacturing hub. Additionally, it is anticipated that the availability of inexpensive labor and beneficial government efforts will accelerate market expansion in the area.

Middle East & Africa: During the course of the forecast period, the moisture curing adhesives market is anticipated to expand significantly in the Middle East & Africa area. The expanding building sector in the area is anticipated to increase demand for adhesives there. Also, the region's market is anticipated to rise as a result of the increased emphasis on infrastructure development and rising investments in the automotive and electronics sectors.

Latin America:

Throughout the forecast period, the market for moisture-curing adhesives is anticipated to expand steadily in South America. The expanding building sector in the area is anticipated to increase demand for adhesives there. In addition, rising investments in the car and electronics sectors are anticipated to support regional market expansion.

In conclusion, the market for moisture-curing adhesives is anticipated to expand significantly throughout the forecast period across all geographies. The need for adhesives is predicted to rise across a range of end-use industries, and there will be an increasing emphasis on environmentally friendly and sustainable adhesives as well as supportive government measures. To be able to make wise business decisions, market participants must grasp the distinct set of elements that each region possesses that affect the market's growth.

Some of the major players in the global moisture curing adhesives market include:

The market is highly fragmented with the presence of numerous players.

The players in the market are focusing on product innovation and expansion of their product portfolio to gain a competitive edge.

The companies are also engaging in partnerships and collaborations to expand their global footprint.

For the purpose of this report, the global moisture curing adhesives market has been segmented based on type, application, and region.

| PARAMETERS | DETAILS |

| The market size value in 2022 | USD 6.0 Billion |

| CAGR (2022 - 2032) | 7% |

| The Revenue forecast in 2032 |

USD 11.03 Billion |

| Base year for estimation | 2022 |

| Historical data | 2020-2021 |

| Forecast period | 2022-2032 |

| Quantitative units |

|

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments covered | By Type Outlook, Application Outlook, Regional Outlook |

| By Type Outlook |

|

| By Application Outlook |

|

| Regional scope | North America; Europe; Asia Pacific; Latin America ; Middle East & Africa |

| Country scope | U.S.; Canada; U.K.; Germany; France; BENELUX; China; India; Japan; South Korea; Brazil; Saudi Arabia; UAE; Turkey |

| Key companies profiled | Henkel AG & Co. KGaA, 3M Company, Sika AG, B. Fuller Company, Bostik SA, Huntsman Corporation, Dow Chemical Company, Avery Dennison Corporation, Wacker Chemie AG, Ashland Global Holdings Inc. |

| Customization scope | 10 hrs of free customization and expert consultation |