Fintech Capital Market Activity in the Middle East and Southeast Asia

Fintech Capital Market Activity in the Middle East and Southeast Asia

The fintech industry in the Middle East and Southeast Asia is poised for strong growth. Innovative payment processors, financial services companies, and digital transaction management platforms are already disrupting the traditional finance sector and are gaining traction in domestic and international financial markets.

Blockchain companies and investments dominated Southeast Asian fintech capital market activity while Middle Eastern investors preferred later-stage investments within the sector. Jahani and Associates (J&A) forecast the continued expansion of Middle Eastern and Southeast Asian fintech companies and capital market activity.

J&A is an international investment bank headquartered in New York City with offices and operations across the Middle East, Southeast Asia, and Central America. J&A specialized in cross-border capital market activity between the regions in which we operate.

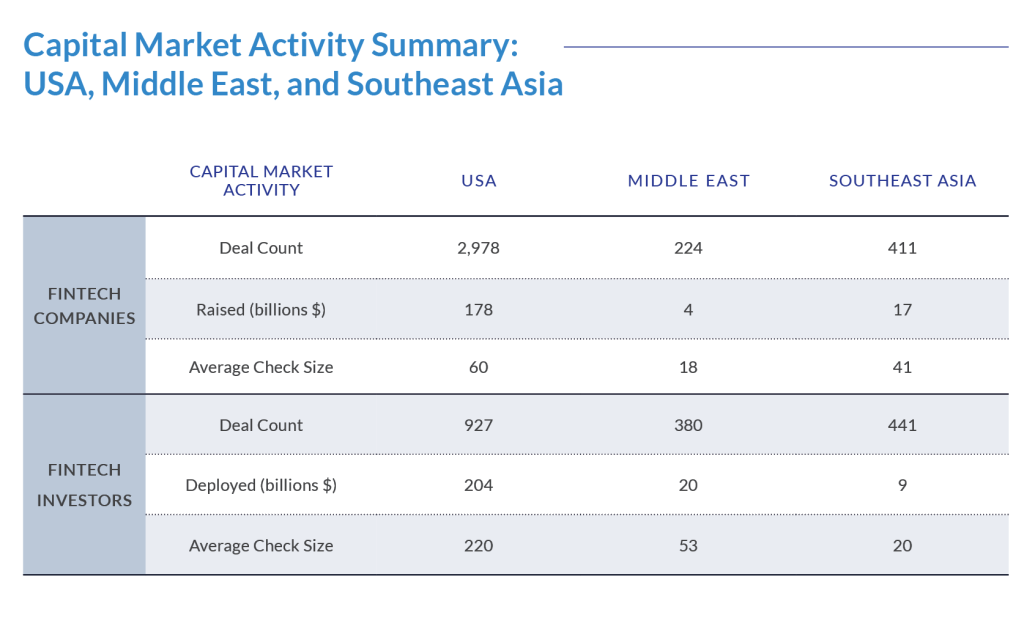

- USA-based fintech companies conducted significantly more capital market activity than their Middle Eastern and Southeast Asian counterparts in 2021. The abundance of capital has accelerated the growth of USA-based fintech companies, but a burgeoning set of growth companies in these emerging markets will drive global fintech capital market activity in 2022 and beyond.

- USA-based fintech companies conducted 2,978 deals in 2021 with a total of $178 billion and a median deal size of $60 million. Middle Eastern and Southeast Asian fintech companies conducted 244 and 411 deals respectively and raised a combined total of $21 billion in 2021.

- USA-based investors have been more active in the fintech sector than Middle Eastern and Southeast Asian investors in 2021 in absolute terms. However, Middle Eastern and Southeast Asian investors conducted significantly higher deal counts in proportion to the number of fintech company deal counts in their domestic markets, demonstrating an appetite for investments.

- Average check size deployed by Middle Eastern and Southeast Asian investors in fintech deals in 2021 was significantly lower than USA-based investors. Early-stage companies in the emerging markets are receiving significant deal flow showing the growth potential of these regions.

- Community management platforms, which include several key blockchain companies, experienced the largest capital deployment in the Middle Eastern and Southeast Asian fintech markets in 2021. Grab dominated deal size with a $5 billion PIPE conducted in December 2021.

- Payment processing services and financial services are growing sectors in both emerging markets and received approximately $5 billion and $2.6 billion respectively. Vietnam Payment Solution conducted a $250 million round in July 2021, the largest transaction in the payment processing sector.

2021 ASEAN Fintech Deals by Month

Fintech companies headquartered in Southeast Asia conducted significant capital market activity in Q4 of 2021. The sector has produced consistent deal flow despite strict economic lockdowns and travel restrictions. Blockchain transaction dominated deal count among the Southeast Asian fintech market. The growth of early-stage venture capital deals in the sector highlights the emergence of new companies in the market and the growth potential of the Southeast Asian fintech sector.

- $17.28 billion was deployed into Southeast Asian fintech companies across 411 deals in 2021 with a median deal size of $5.3 million. December 2021 saw the largest capital deployment of over $5 billion representing approximately 29% of capital deployed over the period.

- The largest deal in the sector was the $750 million acquisition of OVO, a developer and operator of payment and financial services platforms Grab, which was announced on October 4, 2021.

- Cryptocurrency dominated deal count among the Southeast Asian fintech market with 351 deals, or approximately 80%, in the sector where cryptocurrency-related deals focused on seed and early-stage venture capital funding.

- Approximately 34% of capital raised by Southeast Asian fintech companies was deployed into early-stage companies. This showcases the emergence of new companies, an increase in competition, and the growth potential of the sector.

- Mergers and acquisitions, including the acquisition of OVO, raised 21% of capital invested into Southeast Asia despite only seven deals being conducted.

- Sixteen Southeast Asia fintech companies raised late-stage venture capital funding, demonstrating the emergence of mature companies and a well-balanced funding ecosystem.

2021 ASEAN Deal Spotlight: Alami – Sharia Compliant Financing for SMEs

The Company

Alami is an Indonesia-based fintech platform designed to serve small to mid-sized businesses with access to sharia-compliant financing organizations. Alami’s platform provides in-depth data analytics to businesses regarding financing from various institutions allowing them to make informed and up-to-date transactions.

Recent Fundraising

- Alami completed a Series A round of $17.5 million on August 13, 2021, at an undisclosed valuation.

- Quona Capital and EV Growth led the round with Dubai International Financial Center and other undisclosed investors participating.

- Alami had previously raised $24.7 million through three rounds of seed funding.

2021 Middle East Fintech Deals by Month

Fintech companies headquartered in the Middle East have conducted notable capital market activity over 2021 with peaks in April and December. The sector has produced consistent deal flow despite strict economic lockdowns and travel restrictions that have eased and resurged over the year. J&A forecasts continued growth in 2021 Q4 activity into 2022 and beyond.

- In 2021, $4.66 billion was deployed into Middle Eastern companies across 251 deals, with a median deal size of $3.1 million.

- November 2021 saw the largest deal count with 25, but low capital deployment of $400 million representing approximately 8% of capital deployed over the period.

- Notable deals in the sector include the PIPE, private investment into a public company, and subsequent reverse merger of Pagaya, an online lending platform provider, on September 15, 2021.

- Approximately 30% of capital raised by Middle Eastern fintech companies was deployed into early-stage companies.

- Middle Eastern Fintech companies conducted notable IPOs in 2021. The largest IPO was that of the Saudi Stock Exchange (SAU: 1111), on December 8, 2021, in which over $1 billion was raised.

- Mergers and acquisitions, as well as reverse mergers, accounted for 18% of capital market activity in the space. The acquisition of Simplex, the Israeli bitcoin payment processing company, by Nuvei, was one of the largest Middle Eastern fintech acquisitions in 2021.

2021 Middle East Deal Spotlight: Tarabut Gateway Dubai Banking Regtech

The Company

Tarabut Gateway is a Dubai-based financial technology and software development company that has created a platform to regulate the banking sector. The platform is designed to connect a regional network of banks and other fintech companies through a universal applications programming interface (API). Tarabut’s platform utilizes the API to assist in the transfer of data and to create a greater level of integration within the finance sector in the region.

Recent Fundraising

- Tarabut Gateway completed a pre-Series A round of $12 million on November 2, 2021, at an undisclosed valuation.

- Tiger Global Management led the round with Dubai International Financial Centre and other undisclosed investors participating.

- Tarabut Gateway had previously raised $13 million through seed funding in February 2021, which was also led by Tiger Global Management.

2022: What to expect this year

Southeast Asia and the Middle East are two of the world’s best-performing emerging markets. Financial markets are becoming increasingly sophisticated in these regions and the disruption of the traditional financial sector is a trend that will continue and accelerate in 2022.

The cryptocurrency sector experienced a high level of deal flow in Southeast Asia in 2021. Later-stage Middle Eastern fintech companies saw significantly larger capital deployment than early-stage competitors.

Fintech companies should be mindful of the commercial and financial opportunities available in these regions and the appetite that investors in the markets possess for early-stage deals. Companies operating within these markets will continue to grow and become attractive acquisition targets for strategic acquirers looking to enter the market.

J&A forecasts the continued expansion of capital market activity within the Southeast Asian and Middle Eastern fintech markets.