Want to curate the report according to your business needs

Report Description + Table of Content + Company Profiles

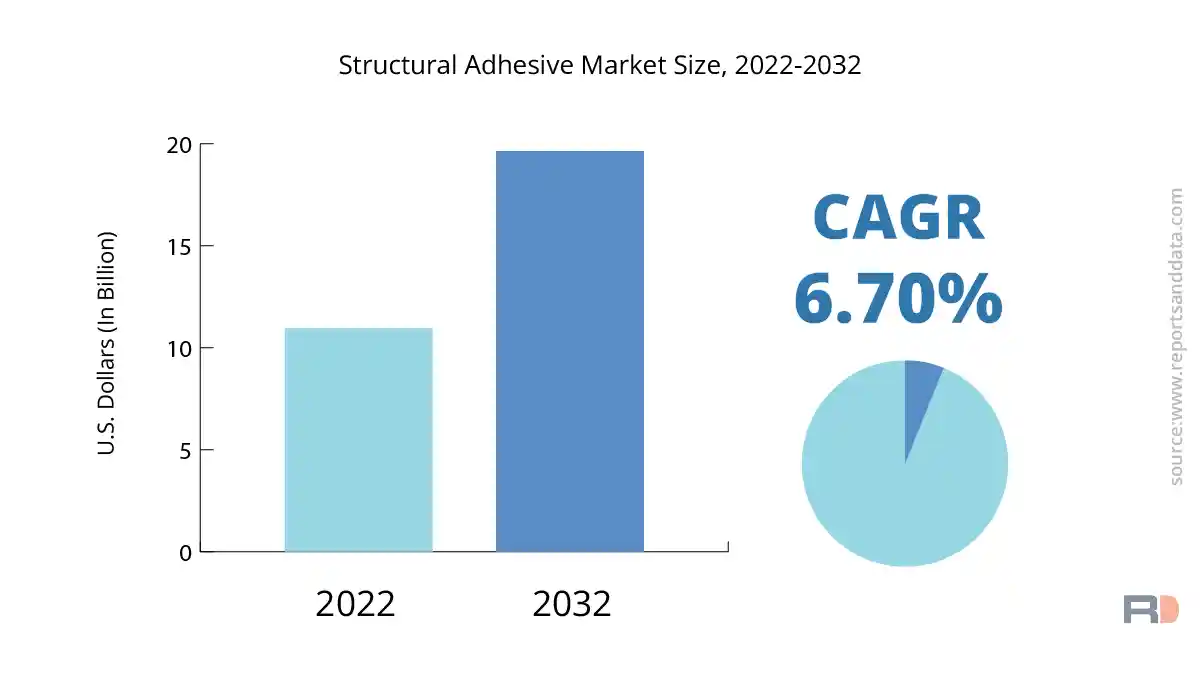

The global structural adhesive market size was USD 10.95 Billion in 2022 and is expected to reach USD 19.63 Billion in 2032, and register a revenue CAGR of 6.7% during the forecast period. The need for high-quality and long-lasting adhesives among consumers is on the rise, and the popularity of lightweight and environmentally friendly adhesives is also on the rise. These and other factors are largely developing the market in the construction and automotive sectors.

The capacity of structural adhesives to deliver high strength, durability, and stiffness, which are essential for improving the performance and safety of vehicles, makes the automotive industry one of the largest end-users of structural adhesives. Body-In-White (BIW) assemblies, sub-assemblies, and panel bonding are just a few of the automobile applications that structural adhesives are employed for. The need for structural adhesives in the automobile industry is expected to rise even more as lightweight vehicles become more popular and carbon emissions become a more pressing issue.

With structural adhesives' great bonding strength and endurance in a range of applications, including the bonding of concrete, metal, and wooden buildings, the construction sector is another significant end-user of these materials. The demand for structural adhesives in the construction industry is expected to expand further as a result of rising demand for infrastructure projects and high-rise structures, particularly in emerging countries.

In addition, the structural adhesive market is expected to expand due to the increased popularity of lightweight and environmentally friendly adhesives. With their capacity to deliver high bonding strength and durability, while also decreasing the weight of the finished product and minimizing environmental effects, lightweight and environmentally friendly structural adhesives are growing in popularity among end-users.

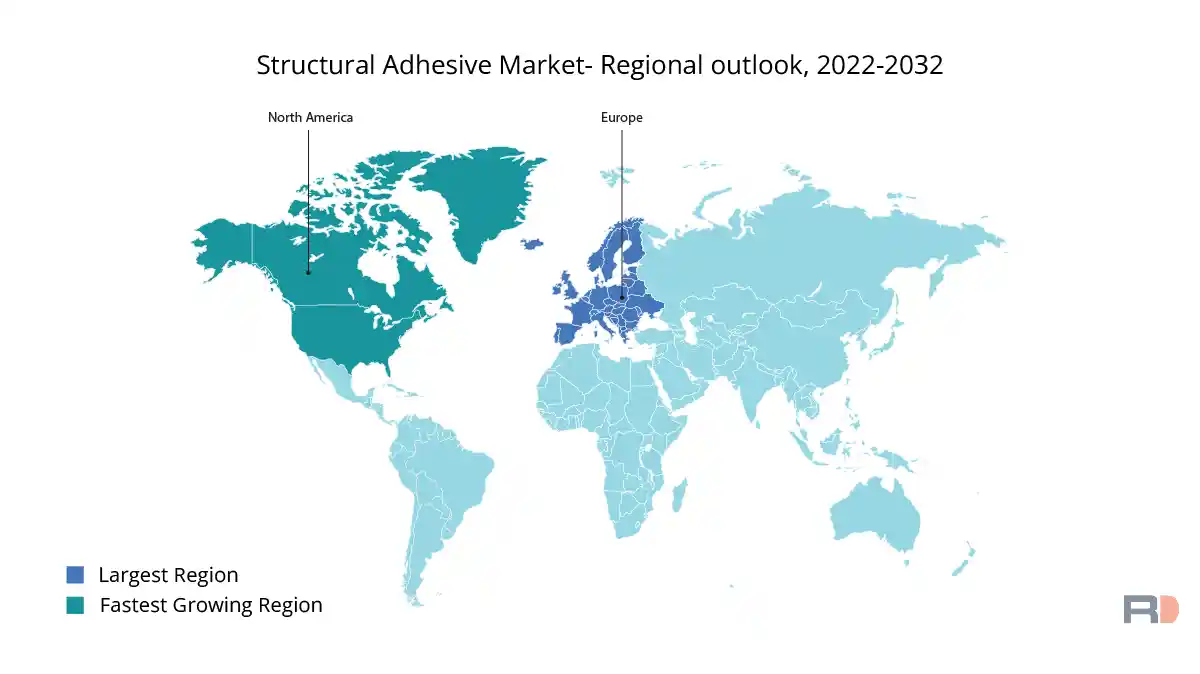

With the presence of important end users including the construction and automotive industries as well as rising demand from developing countries including China and India, the Asia Pacific region is predicted to dominate the structural adhesive market. The structural adhesive market is expected to continue to rise in the Asia Pacific region as a result of rising infrastructure and building project investments in the area and rising consumer demand for lightweight and environmentally friendly adhesives.

However, several issues, including the high cost of structural adhesives in comparison to conventional fastening methods, the lack of end-user awareness of structural adhesives' advantages, and availability of less expensive alternatives, are also expected to restrain market revenue growth. The usage of adhesives in several sectors of the economy, including the food and beverage and healthcare sectors, is also subject to strict laws that are expected to further restrain the market revenue growth.

Manufacturers are putting their efforts into creating novel, economical structural adhesive solutions that address these issues and take into account changing consumer demands. For instance, some producers are creating bio-based, recyclable adhesives with good bonding and durability while simultaneously having a smaller environmental impact. As a way to specifically address the needs and demands of end users, manufacturers are also concentrating on offering tailored solutions and services.

The demand from the construction and automotive industries, consumer preference for strong, long-lasting adhesives, and growing popularity of lightweight and environmentally friendly adhesives are all expected to contribute to the significant growth of the global structural adhesive market during the forecast period. However, several constraints, including structural adhesives' high price and end users' ignorance of their advantages, are also expected to impede market revenue growth.

In 2021, the global structural adhesive market's epoxy segment accounted for the biggest revenue share. Several resin types, such as epoxy, Polyurethane, acrylic, methacrylate, cyanoacrylate, and others, are used to segment the global structural adhesive market. The epoxy sector was one of these, and in 2021 it contributed the most to income. Epoxy adhesives, which are widely used in a variety of industries including automotive, construction, aerospace, and electronics, offer great bonding strength, durability, and chemical and heat resistance. Due to their ability to adhere to a variety of substrates, including metals, polymers, and composites, these adhesives are renowned for their exceptional bonding abilities. Epoxy resin market expansion is anticipated to be fueled by the rising need for high-strength bonding in the automotive and aerospace sectors.

In terms of revenue CAGR, the polyurethane segment is anticipated to grow at the quickest rate. In terms of revenue CAGR throughout the projection period, the polyurethane segment is anticipated to grow at the fastest rate. Its development might be linked to the rise in the demand for energy-efficient products and Lightweight Materials in the building and automotive sectors. In many applications, including the joining of different materials, panel bonding, and sealing, polyurethane adhesives are employed because they have great bonding strength, flexibility, and impact resistance. These adhesives are also well-known for having strong resistance to water, Solvents, and UV light, making them ideal for use in outdoor applications. The market for Polyurethane Resin is anticipated to develop even more as a result of rising demand for environmentally friendly and sustainable adhesives.

During the anticipated term, the acrylic segment is anticipated to increase steadily. During the anticipated term, the acrylic segment is anticipated to increase steadily. Acrylic adhesives are frequently utilized in applications including the bonding of metal, plastics, and glass because they provide good bonding strength and quick cure times. These adhesives are well-known for being shock, vibration, and impact resistant, making them appropriate for usage in the building and transportation sectors. It is anticipated that the growth of the acrylic resin market would be fueled by the rising demand for lightweight materials and the requirement for increased safety in the transportation sector.

Throughout the projected period, the methacrylate segment is anticipated to develop moderately. Throughout the projected period, the methacrylate segment is anticipated to develop moderately. Methacrylate adhesives are frequently utilized in applications like the bonding of metal, polymers, and composite materials because they have a strong bind and cure quickly. These adhesives are well-known for having a high resistance to impact, vibration, and shock, making them appropriate for usage in the building and transportation sectors. It is anticipated that the methacrylate resin market would expand as a result of the rising demand for High-performance Adhesives in the aerospace and electronics sectors.

Throughout the projected period, the cyanoacrylate segment is anticipated to rise just modestly. Throughout the projected period, the cyanoacrylate segment is anticipated to rise just modestly. Metal bonding, Rubber bonding, and the bonding of polymers to one another all use cyanoacrylate adhesives because of their quick curing time. These adhesives are utilized in situations where a quick and strong bond is required because of their high bonding strength. These adhesives can only withstand a certain amount of heat, hence they can't be used in high-temperature applications.

Structural adhesives are high-performance adhesives that are used to affix and link two or more materials together. They offer solutions for strong, long-lasting, and dependable bonding. The automotive & transportation, building & construction, aerospace, marine, wind energy, and other segments have been created within the global structural adhesive market.

In the global market for structural adhesives, the automotive and transportation sector generates the most income. The rising need for lightweight materials, like Aluminum and composites, to increase fuel economy and cut emissions is responsible for the expansion of this market. They are perfect for usage in automotive and transportation applications since structural adhesives offer great bonding options for these materials. Structural adhesives are also used in the assembly of automobiles to reduce the quantity of mechanical fasteners needed, which decreases the weight, cost, and assembly time.

Another important market for the use of structural adhesives is the building and construction industry. The need for structural adhesives is being driven by the expansion of construction activities, especially in emerging nations. The bonding of diverse materials, including metals, concrete, polymers, and wood, is a common usage for structural adhesives in the construction industry. As a result of the improved strength and endurance of the bonding produced by the use of structural adhesives in construction, maintenance and repair expenses are decreased.

The segment in the aerospace industry is anticipated to increase at the fastest rate throughout the forecasted period. Since they offer greater strength and endurance than conventional mechanical fastening techniques, structural adhesives are frequently utilized in aerospace applications to bond composite materials. Structural adhesive demand is being driven by the rising demand for lightweight materials, such composites, in aerospace applications.

Another significant area of application for structural adhesives is the maritime and wind energy sectors. Structural adhesives are good bonding solutions for materials exposed to hostile environments, such as saltwater and extremely high or low temperatures, and are used in maritime applications. Structural adhesives, which offer high-strength and dependable bonding solutions, are utilized to join numerous components, including blades and nacelles, in wind energy applications.

Electronics, medical equipment, and sporting goods are a few other industries that use structural adhesives. As a result of the superior bonding solutions offered by structural adhesives in various applications, the goods' durability and dependability are increased.

The structural adhesive market is dominated by Asia-Pacific, which generates the most revenue. The demand for structural adhesives in a variety of applications is being driven by the region's developing economies, such as those of India and China, where industrialization and urbanization are on the rise. The structural adhesive market is expanding as a result of the region's growing use of lightweight materials like composites in the building, automotive, and aerospace industries. The demand for structural adhesives used in air conditioning applications is also anticipated to increase due to the availability of affordable packaged and room air conditioners in the Asia Pacific region, driven by the growing e-commerce sector and discounts provided on online platforms.

Over the projected period, North America is expected to grow at the quickest rate in terms of revenue compound annual growth (CAGR). The adoption of structural adhesives in numerous industries, including the automotive, aerospace, construction, and electronics industries, is being fueled by the region's growing focus on energy efficiency and sustainability. The market for structural adhesives in air conditioning applications, such as smart air conditioners for smart homes, is predicted to experience substantial development in North America due to the growing awareness of global warming and the need for energy-efficient solutions. Manufacturers in the area are utilizing cutting-edge technology, such as the Internet of Things (IoT) and Machine Learning (ML), to produce creative structural adhesive solutions for applications in home heating and air conditioning.

The worldwide structural adhesive market is anticipated to develop moderately in Europe. Demand for structural adhesives in the region is being driven by the industrial and food and beverage sectors, particularly in the UK. The UK's food and beverage industry makes a sizeable contribution to the country's economy, and this business is using more structural adhesives to maintain a constant temperature in structures including buildings, warehouses, and transportation vehicles. The adoption of structural adhesives in additional industries including construction, automotive, and aerospace is another factor that is anticipated to fuel market expansion in Europe.

Some of the major companies included in the global structural adhesive market report are:

For the purpose of this report, the global structural adhesive market has been segmented by resin type, application, and region:

| PARAMETERS | DETAILS |

| The market size value in 2022 | USD 10.95 Billion |

| CAGR (2022 - 2032) | 6.7% |

| The Revenue forecast in 2032 |

USD 19.63 Billion |

| Base year for estimation | 2022 |

| Historical data | 2020-2021 |

| Forecast period | 2022-2032 |

| Quantitative units |

|

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments covered | By Resin Type Outlook, Application Outlook, Regional Outlook |

| By Resin Type Outlook |

|

| By Application Outlook |

|

| Regional scope | North America; Europe; Asia Pacific; Latin America ; Middle East & Africa |

| Country scope | U.S.; Canada; U.K.; Germany; France; BENELUX; China; India; Japan; South Korea; Brazil; Saudi Arabia; UAE; Turkey |

| Key companies profiled | Henkel AG & Co. KGaA, 3M Company, Sika AG, The Dow Chemical Company, Huntsman Corporation, Lord Corporation, Arkema Group, Ashland Global Holdings Inc, Scott Bader Company Ltd, Hubei Huitian Adhesive Enterprise Co. Ltd, Pidilite Industries Limited |

| Customization scope | 10 hrs of free customization and expert consultation |